The Basics of Running a Legally Sound Church Business Meeting

Attorneys Richard Hammar and Sarah E. Merkle discuss best practices for implementing and following parliamentary procedures.

Attorneys Richard R. Hammar and Sarah E. Merkle

Loading the player...

Churches should select and implement a specific body of parliamentary procedure in order to efficiently consider business and properly make legally sound decisions.

Yet some churches have not adopted procedures, while others do not recall what they have adopted—and still others know the procedures they adopted, but do not know if they correctly follow them. This uncertainty leaves many congregations open to the possibilities of disorganized meetings, haphazard decision-making—and possible legal scrutiny down the road.

In this webinar featuring attorneys Richard Hammar and Sarah Merkle—two well-respected voices on the topics of church governance and business meetings—participants will learn more about:

the processes of adopting procedures;

the various types of procedures available to adopt (including Hammar’s analysis of the new 12th edition of Robert’s Rules of Order Newly Revised);

the best practices for implementing and following those procedures;

and more.

Download the presentation slides to follow along and take notes as you watch.

More on this topic:

Make note of 17 Changes Relevant to Churches in Newest Robert’s Rules of Order.

Learn more about what churches need to know to conduct legally sound meetings from this recommended reading collection.

Gain new ideas, insights, and advice on how to proceed as you shift more ministry online.

Find out about the emergency provision you should consider including in your bylaws.

Image: getty/RapidEye

Every Church Is at Risk for Fraud. Here’s Why.

Church Law & Tax’s nationwide survey shows churches of all sizes, ages, and locations are susceptible to financial misconduct.

A nationwide survey of more than 700 church leaders conducted by Church Law & Tax shows nearly one-third serve in congregations that have suffered from some form of financial misconduct.

Among those experiencing it, half said an incident occurred within the past 10 years.

Prior research conducted by other organizations throughout the past 20 years has usually pegged the figure closer to 10 percent or 15 percent for houses of worship. Still, church financial experts have long estimated that the figure was at least one-third or even higher for all congregations across the nation—a figure that appears to track closely with the Church Law & Tax study from 2021.

“It was disheartening to see 30 percent of churches responding had experienced fraud,” said CPA Vonna Laue, a senior editorial advisor for Church Law & Tax who co-led the survey project. “It did confirm to me how prevalent this situation is in churches.”

Churches of all sizes, ages, and locations are susceptible, according to the survey’s findings—and fraud prevention experts say the vulnerabilities that perpetrators commonly exploit are ones easily remedied.

“The primary types of financial misconduct that occurred are the most preventable with a good internal control structure,” Laue said.

Yet many churches do not install simple safeguards out of a perceived high level of trust among their ranks, a noted frustration among the financial experts who reviewed Church Law & Tax’s results and provided comment.

“It will never happen here”

Two-thirds of survey respondents who said they weren’t aware of fraud in their churches also said they believe the problem is unlikely or “will never” happen in their churches. Ironically, among those who endured misconduct, half said they shared a similar “it-will-never-happen” sentiment before uncovering a case—and 80 percent then implemented several basic measures after the fact.

“This is one of the most important takeaways from this study,” noted Rollie Dimos, a Certified Fraud Examiner (CFE) and author of Integrity at Stake: Safeguarding Your Church from Financial Fraud. “Most people think that their church is immune from the risk of fraud because [their] staff and volunteers are trustworthy. . . . We trust people to do the right thing, but we can fail them if we don’t hold them accountable or provide controls to protect them.”

Nathan Salsbery, a CFE and a partner and executive vice president for nonprofit CPA firm CapinCrouse, said many congregations “do not implement effective internal controls until they feel the pain of fraud firsthand.”

Salsbery is currently assisting fraud investigations at three different churches. “Had these churches implemented a few basic internal controls, they would have either prevented the fraud or would have detected it much sooner,” he added.

A costly toll

The failure to prevent or quickly detect financial misconduct exacts heavy tolls on congregations. In a 2022 study, Gordon-Conwell Theological Seminary’s Center for the Study of Global Christianity estimates church fraud globally will total $70 billion a year by 2025.

The fallout extends beyond pure dollars, though, and often with devastating effects. In an analysis of the language used by respondents to Church Law & Tax’s survey, words associated with anger and sadness appeared repeatedly among respondents who experienced fraud.

“The financial losses can be staggering,” Salsbery said. “While the financial losses are bad enough, there are usually many other losses that result from the inevitable broken trust and relationships damaged by such long-term acts.”

Such damage is understandable, given the typical identity of the perpetrator and the amounts that he or she steals.

As the Church Law & Tax research shows, the profiles of offenders frequently included treasurers, board members, and middle-aged pastors. Financial losses were the largest among perpetrators with long tenures at their churches (see “Loved and Trusted: What Shocks Us Most about Fraud Perpetrators”).

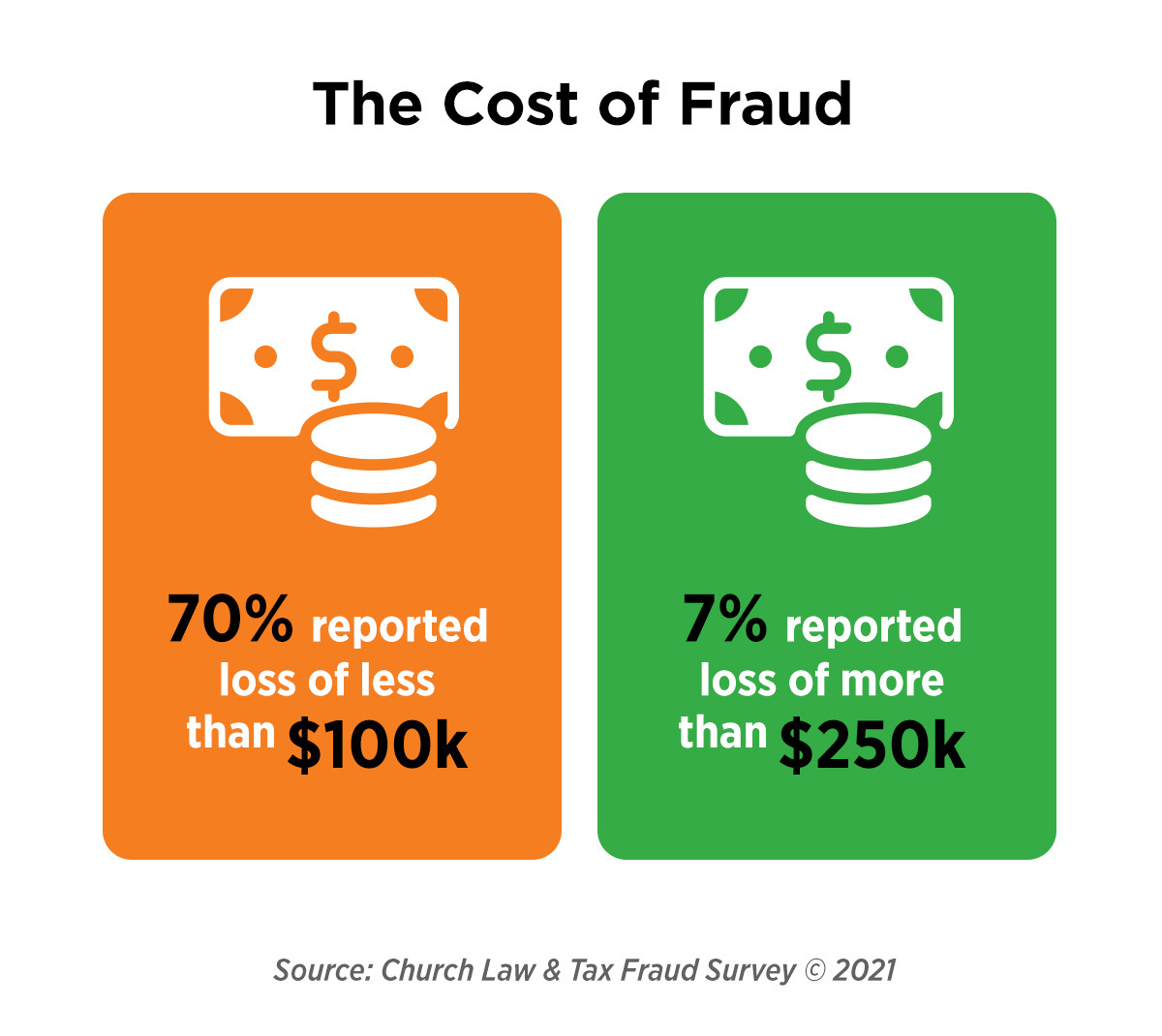

As for the amounts stolen, Church Law & Tax’s research showed 69 percent of those victimized said their losses measured less than $100,000. About 14 percent said the amounts topped $100,000, while another 15 percent said they did not know how much was taken.

Precise financial losses are difficult to pinpoint since the perpetrator may not know or may lie. And churches that choose not to contact law enforcement likely will miss out on learning the full extent because a thorough investigation never happens. Nearly 70 percent of victimized churches chose not to report their cases to police. Overall, only 22 percent of all respondents said their boards would contact law enforcement in the event a future suspected or actual case arose (see “Reporting Financial Crime as a Matter of Stewardship”).

Easy opportunities

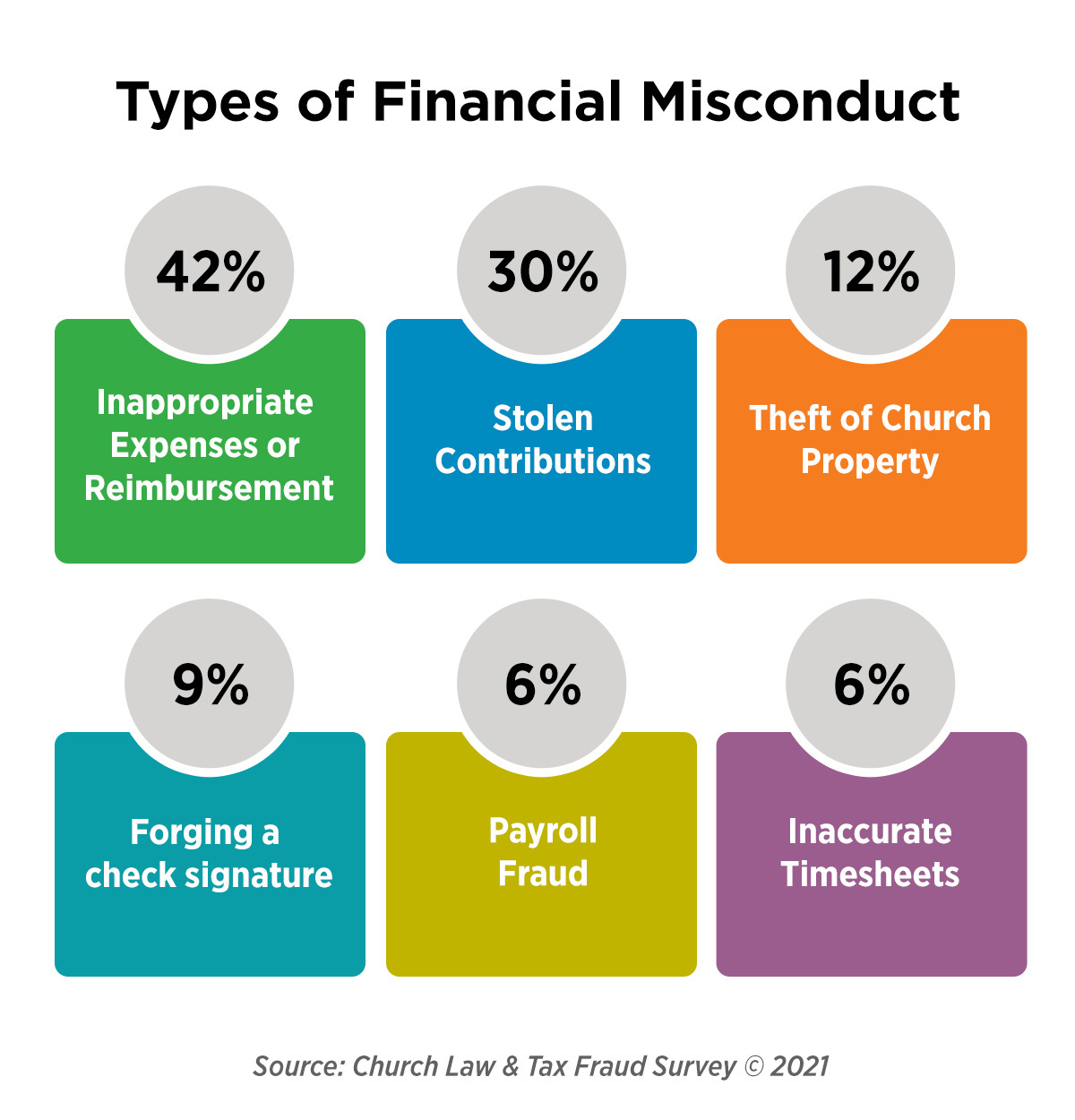

Nearly 42 percent of cases involved “inappropriate expenses or inappropriate expense reimbursements,” the survey showed. Slightly more than 30 percent involved stealing contributions. Payroll fraud and inaccurate timesheets combined constituted 12 percent of the cases. And another 11 percent took tangible church property, while about 9 percent forged check signatures. (Note: Respondents to the “Types of Financial Misconduct” infographic were asked to check all that apply.)

While the type of theft men and women committed against their churches varied, according to the survey, it generally boiled down to one thing: easy opportunities.

“While TV shows often depict fraud as grand and complicated schemes, most fraud committed in the church is simply an individual taking advantage of a situation where no one is looking,” Salsbery observed.

Just assigning another set of eyes to monitor a variety of financial activities could greatly reduce easy opportunities. For instance, the leading “red flag” for persons who committed fraud was excessive control over his or her duties or an “unwillingness to have others cover his/her job duties.”

“Nearly half of fraud schemes found were detected as a result of another employee performing a person’s duties” in their absence, noted CPA Michael Batts, another Church Law & Tax senior editorial advisor who reviewed the results. “The rotating duties of workers performing certain financial duties is, itself, an effective internal control mechanism, especially where adequate segregation of duties for a particular position is not in place.”

Encouraging signs—but much room for improvement

While the ease with which perpetrators stole from their churches is troubling, many of the practices best positioned to thwart such efforts do not require extensive time or expense.

On an encouraging note, many respondents indicated at least some best practices are already in place.

About 86 percent of all respondents regularly generate and review financial statements, and 83 percent make certain two unrelated people work together to handle financial tasks.

Around three-quarters of those who had experienced fraud said they use separate individuals—the “segregation of duties” in accounting parlance—for authorizing cash disbursements, maintaining custody or control over cash, and handling accounting responsibilities. (Note: Most of those who responded to the question about “segregation of duties” were in churches that had experienced fraud. Respondents highlighted in the “Top measures churches take to prevent financial misconduct” infographic were asked to check all that apply.)

Still, the responses for these categories show between 17 percent and 25 percent of churches are not performing these basic measures.

The percentages worsen when considering other areas of financial accountability or internal controls recommended by experts. For instance:

Slightly more than half of respondents said one person in their church has the ability to perform all aspects of cash disbursements without requiring another individual’s involvement. “That is a staggering statistic,” Laue noted.

Dimos said this problem, along with improper expenses or expense reimbursements—the leading type of fraud found in the survey—can be easily prevented by “[r]equiring a second person to review and approve all credit card purchases or reviewing invoices or reimbursement requests before signing checks.”

Additionally, “disciplined monthly reviews of cancelled checks (or images) and reviews of monthly credit card statements and related documentation and support [can] significantly reduce risk,” Salsbery said.

Only one-third of churches store their collections in a safe and secure manner and require dual controls for access when they cannot be immediately deposited at the bank (again, stolen contributions constituted the second-highest type of fraud in the survey).

Only one-third of churches have their payroll approved by someone other than the preparer and then reconciled to the church’s accounting system.

Only 22 percent apply accounting procedures to tangible property susceptible to theft, such as electronic equipment or bookstore inventories.

“The addition of internal controls to protect your church will not cost the church anything,” Dimos observed. “Having a second person—like a staff member, trusted volunteer, or board member—be responsible to review the bank reconciliation and bank statements, or review a general ledger detail report, can provide a great deal of accountability, but not add any extra expense for the church.”

Audits and assessments

Financial audits and fraud risk assessments offer additional protections for churches, although unlike the previously mentioned preventive steps, these typically come with a cost.

An ongoing audit process “can help a church greatly reduce the risk of misappropriation and embezzlement,” Batts said. Dimos agreed, adding the use of fraud risk assessments can go one step further and “help a church test their controls and identify potential weaknesses and risk areas.”

In the survey, about 24 percent of respondents conducted outside audits with a CPA, which involves documentation and third-party support of the financial information, Laue said. Thirty percent hired a CPA or financial expert to perform a less intensive outside review, which relies on inquiries and analytical procedures, Laue noted. Almost 38 percent said they perform internal audits using church staff and volunteers.

In terms of fraud risk assessments, nearly 51 percent said they do not use them at all.

Learning from “hard lessons”

Church Law & Tax’s survey “presents a strong case for churches to be proactive in preventing fraud,” Dimos said.

The fact that 30 percent of churches reported experiencing financial misconduct at some point, and that the possibility exists even more experience it without realizing it, reveals “the risk of fraud is very real in all churches,” Salsbery said.

While many will think the steps are unnecessary, or shouldn’t be necessary because people should know better, Salsbery pointed to examples of fraud contained in the Bible—including Judas’s thefts from Jesus and the disciples’ ministry account or Ananias and Sapphira’s attempt to deceive Peter—as reminders that anyone can succumb to temptation.

“Just as policies are put in place to help prevent other sins from damaging the church, controls are needed to protect churches from the sin of fraud,” Salsbery said.

And taking time now to review practices and strengthen them—especially when no apparent problem exists—only ensures church leaders are stewarding resources well, Laue added.

“Let’s learn from the hard lessons of others,” Laue said. “I strongly encourage churches to take the step and carefully review internal controls or even hire someone to help assess and implement better internal controls now. Even if fraud was never to occur, it won’t hurt for us to operate with good processes in place.”

NEW! Safeguarding Your Church’s Finances—a multi-session video course for pastors, board members, staff, and volunteers on the basics of fraud prevention. LEARN MORE!

Matthew Branaugh is an attorney and editor for Church Law & Tax.

Image: getty/bymuratdeniz

Reporting Financial Crime as a Matter of Stewardship

Reporting financial crime in your church is a matter of stewardship, yet many church leaders report not doing so, or even knowing how.

Reporting financial crime is a matter of stewardship, yet nearly 70 percent of churches that have experienced fraud chose not to report it to the police, according to a 2021 survey of more than 700 church leaders.

The spring 2021 study on financial misconduct surveyed 706 church leaders.

About one-third of leaders said financial misconduct had taken place in their churches. Among those churches that experienced fraud, only a third filed a report with law enforcement.

In my own experience, the vast majority of churches that know or believe financial misconduct occurred are reluctant to contact law enforcement.

These leaders told me they would rather handle the matter internally. Church Law & Tax’s nationwide survey confirms this.

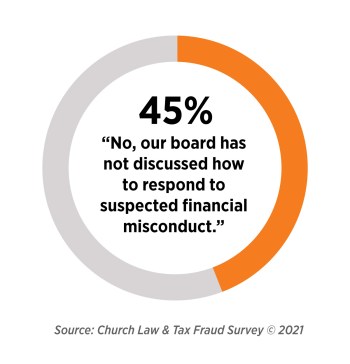

Additionally, nearly half of the respondents said their church boards have not discussed how they would respond to suspected fraud.

Why leaders do not report financial crimes

In the survey, leaders most frequently gave these explanations as to why they did not contact authorities:

We were able to recover the money without having to take legal action (27.7 percent).

We wanted to work on restoration with the individual(s) (26.5 percent).

We did not want to make it public to protect the church’s reputation (20.5 percent).

The church chose to forgive rather than report to the authorities (19.3 percent).

We did not want to make it public to protect the individual(s) (16.9 percent).

Legal action would go against the church’s ministry philosophy (7.2 percent).

(Note: Respondents were asked to check all that apply.)

When I speak with church leaders, their hesitations for contacting law enforcement often arise because the suspected embezzler is almost always a trusted member or employee, and church leaders are reluctant to accuse such a person without irrefutable evidence of guilt.

Seldom does such evidence exist. The pastor may confront the person about the suspicion, but the individual will often deny any wrongdoing—even if guilty. This only increases the frustration of church officials who do not know how to proceed.

Thinking of not reporting a financial crime?

Caution 1: The fraud is often far greater than the church realizes. A failure to report a financial crime may hide the true depth and extent of the crime committed. CPA Vonna Laue’s experience certainly affirms this. “Each time I have been brought into a ministry’s financial fraud situation, the amount of loss grew as more information was uncovered,” said Laue, a Church Law & Tax senior editorial advisor who advised this nationwide survey project. “It was always more than the perpetrator indicated and sometimes even they were surprised by the total.”

Caution 2: It does not matter whether the embezzler intended to pay back the embezzled funds someday. This intent in no way justifies or excuses the crime. The crime is complete when the funds are converted to one’s own use—whether or not there was an intent to pay them back.

Of course, an offender’s repayment may make it less likely that a prosecutor will prosecute the case. And even if the embezzler is prosecuted, this evidence may lessen the punishment. But the courts have consistently ruled that an actual return of embezzled property does not purge the offense of its criminal nature or absolve the embezzler from punishment for his or her wrongdoing. Also, note that church officials seldom know if all embezzled funds are being returned. They are relying almost entirely on the word of the thief.

Caution 3: Whether a church opts to notify law enforcement or not, there are tax law obligations with the Internal Revenue Service (IRS) that must be fulfilled.

Responding to suspected cases of fraud

Church leaders often learn of suspected financial misconduct because discrepancies or irregularities arise or someone submits a tip.

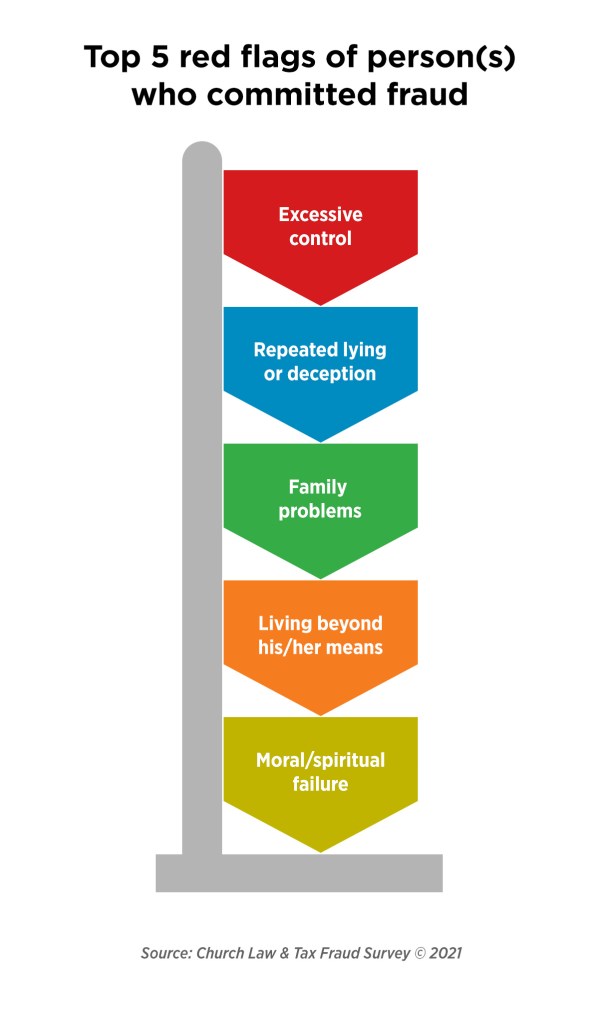

Top Six Red Flags

The survey indentified these signs that someone might be committing fraud:

1. Excessive control or unwillingness to have others cover his/her job duties

2. Repeated lying/deception

3. Family problems

4. Living beyond his/her means

5. Other moral or spiritual failures.

6. High levels of debt (e.g., credit card, student loans)

Along with these red flags, consider the following scenarios that point to the possibility that fraud might be taking place:

Giving is always higher when the person who usually does the counting is on vacation or ill during a weekend service.

A church bookkeeper lives a higher standard of living than is realistic given her or her income.

Church offerings have remained constant, or increased slightly, despite that attendance has steadily increased.

A church official with sole signature authority on the church checking account has purchased a number of expensive items from unknown companies without any documentation to prove what was purchased and why.

Safeguarding Your Church’s Finances—a multi-session video course for pastors, board members, staff, and volunteers on the basics of fraud prevention. LEARN MORE!

When unusual activity gets detected, or a tip is received, church leaders should take these steps in response:

1. Carefully gather information before reporting a financial crime

When evidence of actual or suspected financial misconduct surfaces, the pastor and/or church leaders should gather as much information as possible. Compile all documents and records that point to the possible irregularities and inconsistencies. The church should contact its attorney. It also should strongly consider hiring a qualified CPA firm or Certified Fraud Examiner (CFE) to conduct a more thorough investigation.

Note. Some churches have used CFEs to detect embezzlement and estimate the amount of loss. But note that CFEs are not required to be CPAs, and many have far less familiarity with accounting records than a CPA. The ideal professional would be a CPA who is also a CFE. For more information on CFEs, and to find one nearby, go to the website of the Association of Certified Fraud Examiners.

A deeper investigation offers the best way to quickly determine if the irregularities and inconsistencies are a product of human error or misconduct, and the amounts of money lost. If the cause is error, then the church can address the problem while avoiding making any erroneous and harmful accusations. If the cause is misconduct, then the church knows it must take appropriate next steps in whether to report a financial crime.

2. Sit down with the suspected perpetrator

If sufficient information points to a suspected perpetrator, at least two church leaders, and possibly the church’s attorney and the CPA or CFE (if one is hired) should meet with the person. Provide some general descriptions about the irregularities or inconsistencies that have arisen and ask the person what they can tell you about them. Take careful notes, including any questions or comments the person makes.

If the person confesses and asks how things will be handled, explain the criminal nature of the offense. Also explain the legal requirements to contact the IRS (see more below).

Caution. Always keep in mind that embezzlement is a criminal offense. Depending on the amount of funds or property taken, it may be a felony that can result in a sentence in the state penitentiary.

If the person confesses, evaluate with the church’s attorney the possible ways the person can possibly repay the stolen funds—but know that such a step does not absolve the person of his or her crime, nor does it eliminate potential consequences with the IRS. Also know upfront that such agreements by embezzlers to repay funds often are not honored.

3. Contact authorities

If there is a confession, or if the evidence clearly indicates the person stole church funds, church leaders must consider turning the matter over to the police or local prosecutor and the IRS. These are very difficult decisions, since doing them may result in the prosecution, penalization, and possible incarceration of a member of the congregation.

Note. Embezzlers never report their illegally obtained “income” on their tax returns. Nor do they suspect that failure to do so may subject them to criminal tax evasion charges. In fact, in some cases. it is actually more likely that the IRS will prosecute the embezzler for tax evasion than the local prosecutor will prosecute for the crime of embezzlement. Along with contacting local authorities, your church also should contact the IRS regarding the matter.

Before you “forgive and forget”

In some cases, a person confesses to the misconduct. Often, this is to prevent the church from turning the case over to the police or the IRS. Perpetrators believe they will receive “better treatment” from their own church than from the government. In many cases, they are correct.

It often is astonishing how quickly church members will rally in support of the embezzler once he or she confesses—no matter how much money was stolen from the church. This is especially true when the perpetrator used the stolen funds for a “noble” purpose, such as medical bills for a sick child.

Many church members demand forgiveness for the perpeator. The idea of turning the perpetrator over to the authorities is both shocking and repulsive. But is it this simple? Should church leaders join in the outpouring of sympathy? If the embezzler confesses, should church leaders leave it at that?

These are questions that each church will have to answer for itself, depending on the circumstances of each case.

Before forgiving the embezzler and dropping the matter, though, church leaders should consider the following.

Embezzlement is a crime breaches a sacred trust

The church should insist, at a minimum, that the embezzler must:

disclose how much money was embezzled,

make full restitution by paying back all embezzled funds within a specified period of time, and

immediately and permanently be removed from any position within the church involving access to church funds.

Closely scrutinize and question the amount of funds the embezzler claims to have taken. Remember, you are relying on the word of an admitted thief. That is why it is important to involve the church’s attorney, as well as a CPA or CFE, when suspicions first arise.

The embezzler must return the stolen money within a specific time or sign a promissory note agreeing to pay back the funds within a specific time.

Caution. An attorney should be consulted before the church has any discussions about an agreement with the embezzler about paying back stolen funds.

The church faces tax consequences for not reporting financial crime to IRS

The church needs to tell the embezzler that the stolen money is taxable income. Therefore, failure to agree to either of the above alternatives will force the church to issue him or her a 1099 (or a corrected W-2 if the embezzler is an employee) reporting the embezzled funds as taxable income.

If funds were embezzled in prior years, then the employee will need to file amended tax returns for each of those years to report the illegal income since embezzlement occurs in the year the funds are misappropriated.

Failure to report taxable income will subject the church to a potential penalty (up to $10,000) for aiding and abetting in the substantial understatement of taxable income under section 6701 of the tax code.

Note. If an employer is able to determine the actual amount of embezzled funds as well as the perpetrator’s identity, the full amount may be added to the employee’s W-2, or it can be reported on a Form 1099 as miscellaneous income. But remember, do not use this option unless you are certain that you know the amount that was stolen as well as the thief’s identity.

If the full amount of the embezzlement is not known with certainty, then church leaders have the option of filing a Form 3949-A (“Information Referral”) with the IRS. Form 3949-A is a form that allows employers to report suspected illegal activity, including embezzlement, to the IRS. The IRS will launch an investigation based on the information provided on the Form 3949-A. If the employee in fact has embezzled funds and not reported them as taxable income, the IRS may assess criminal sanctions for failure to report taxable income.

Caution. If the embezzler agrees to pay back the stolen money and does so, does this convert the embezzled funds into a loan, thereby relieving the employee and the church of any obligation to report the funds as taxable income in the year the embezzlement occurred? The answer is no.

Most people who embezzle funds insist that they intended to pay the money back and were simply “borrowing” the funds temporarily. An intent to pay back embezzled funds is not a defense to the crime of embezzlement.

The courts are not persuaded by the claims of embezzlers that they intended to fully pay back the funds they misappropriated. The crime is complete when the embezzler misappropriates the church’s funds to his or her own personal use.

There is yet another problem with attempting to recharacterize embezzled funds as a loan. If the church enters into a loan agreement with the embezzler, this may require congregational approval. Many church bylaws require congregational authorization of any indebtedness, and this would include any attempt to reclassify embezzled funds as a loan. Of course, this would have the collateral consequence of apprising the congregation of what has happened.

Reporting financial crime may be a matter of fiduciary responsibility and good stewardship

Viewing the offender with mercy does not mean forgiving the debt and ignoring the crime. Churches are public charities that exist to serve religious purposes.

Donors give money in support of those purposes.

Forgiving and ignoring embezzlement may not serve those purposes.

The church should care about other churches

As Church Law & Tax’s findings also reveal, the average tenure of embezzlers tended to be less than 10 years, and oftentimes measured less than 5 years.

Letting an offender off the hook and sending them on their way exposes other churches to the same behavior. No record of the offender’s activities will be available—and that means even a church that follows healthy screening and selection steps (including criminal background checks) will be unable to detect this person’s past offenses.

As Laue, the CPA who advised the survey project, also notes: “We have a responsibility to protect Kingdom resources, whether they are ours or someone else’s, and we can’t do that if we don’t take the necessary steps to make others aware of the fraudulent activity.”

The bottom line: Churches should report financial misconduct as an act of stewardship for the global church.

Case Study: A Repeat Embezzler. A church administrator embezzled over $350,000 from his church. He wrote unauthorized checks to himself and others from the church’s accounts, and used the church’s credit card on over 300 occasions to purchase personal items. Police officers were called and he made a full confession.

The church secured a $1 million civil judgment against him. He was prosecuted and convicted on four felony counts including forgery and theft, and he was sentenced to 32 years in prison based on “aggravated circumstances” (the large amount of money that had been stolen, the care and planning that went into the crimes and their concealment, the fact that a great number of checks were stolen and unauthorized credit card charges made, and breach of trust).

Several years earlier, the administrator embezzled a large amount from a prior church employer. However, that church chose not to initiate criminal charges, believing that he had learned his lesson.

This case study is taken from the “Embezzlement” section of the Legal Library.

Answers to other key questions about reporting financial crimes

Find detailed answers to the following questions about embezzlement in the Legal Library:

How does embezzlement occur?

How does a pastor handle someone who confesses to embezzlement during a confidential counseling session?

Can a church require a suspected embezzler to take a polygraph test?

How can a church avoid making false accusations?

How should a church discuss embezzlement with the congregation?

And as both the study and my own experience show, a most-troubling aspect of financial misconduct in churches is the unfortunate reality that many pastors and other leaders choose to handle fraud or suspected fraud internally—meaning they avoid involving a CPA or CFE, the IRS, and law enforcement. But the failure to report can be problematic for the reasons I have detailed in this article.

For the sake of practicing good financial stewardship, it is my hope and prayer that churches will carefully consider the advice I offer in this article. Most importantly, my hope is that churches will seek do all they can to prevent financial misconduct from happening in the first place through implementing a system of sound internal control.

Attorney Matthew J. Branaugh, content editor for Church Law & Tax, contributed to this article.

Richard R. Hammar is an attorney, CPA and author specializing in legal and tax issues for churches and clergy.

Image: AdobeStock/Pixel-Shot

Loved and Trusted: What Shocks Us Most About Fraud Perpetrators

A closer look at the men and women who steal from churches—and the red flags leaders should watch for.

Church Law & Tax’s nationwide survey of congregations and the financial misconduct they experience paints four portraits of the types of individuals who most commonly steal from their churches.

What’s most shocking?

The positions of trust the men and women who commit these crimes carry.

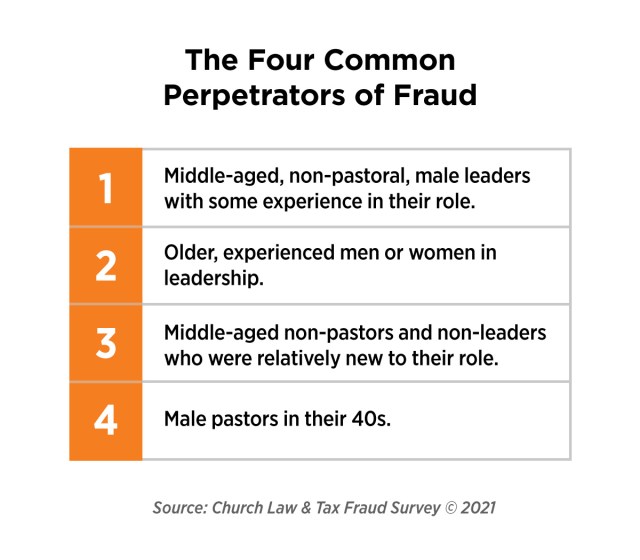

The study revealed that common perpetrators included middle-aged men who served as treasurers or board members, sometimes for upwards of 10 years; men and women in their 30s and 40s who worked in their roles as administrators and treasurers for less than 5 years; and male pastors in their 40s.

And then there’s the group of perpetrators that may be the most surprising of all: men and women, typically 60 or older, who held their positions for 20 years or more. The crimes committed by these individuals “were disproportionately expensive” compared with other offenders, according to Arbor Research Group, the firm Church Law & Tax commissioned to survey church leaders nationwide.

“Just as fraud can happen in any sized church, fraudsters can be any age, any gender, and perform any function in the church,” said Rollie Dimos, a Certified Fraud Examiner (CFE) who reviewed the survey results ahead of publication and provided comment. “That’s why it is so important to put financial processes in place to actually protect our church team members from being tempted to steal God’s money. Internal controls are like guardrails that help keep people honest and accountable.”

Portraits of the perpetrators

The national survey fielded responses from 706 leaders and revealed nearly 30 percent served in churches that had experienced some form of financial misconduct. Nearly half said the crimes occurred within the past 10 years (see “Every Church Is at Risk for Fraud. Here’s Why”).

Those who suffered from some form of fraud answered questions exploring the acts committed and the people responsible for them. Through those responses, Arbor was able to classify the four classes of perpetrators, shedding more light on the common traits they possess.

Class 1

Arbor characterized this group as “middle-aged, non-pastoral male leaders with some experience in their roles.” These men frequently served as treasurers, board members, or in non-pastoral leadership roles.

Class 2

This group constituted “older, experienced men or women in leadership,” Arbor noted. They often served in their roles—which varied—for 20 years or more. A quarter of these cases resulted in losses of $250,000 or more, while half caused losses ranging anywhere from $10,000 to $250,000.

“The worst-case scenario for a church is to have fraud committed by long-tenured leaders in the church,” said Nathan Salsbery, a CFE and a partner and executive vice president for nonprofit CPA firm CapinCrouse who also previewed the survey results. “And if those leaders had unmonitored access to the cash coming in, the cash going out, and the accounting records, the financial losses can be staggering.”

More on Those Who Embezzle

Find additional examples of people steal from churches and how they do so—along with the consequences of such theft and ways to prevent and respond to it—see the “Embezzlement” section of Church Law & Tax’s Legal Library.

Class 3

This class featured the highest number of perpetrators, Arbor said. It, too, was evenly represented by men and women, but their ages ranged from 30 to 49 and their average tenures were 5 years or less. Among these individuals, about one-third worked as administrators, while 20 percent served as treasurers. Overall, 20 percent were unpaid volunteers.

Class 4

This group was comprised entirely of male pastors “typically 40 to 49 years of age and in their role 1 to 5 years,” Arbor noted. The thought of a pastor betraying his congregation in this way exacts significant tangible and intangible damage, Salsbery noted. “Lack of healthy accountability for senior leadership is one of the most significant risks to a church,” he said.

Red flags to monitor

The top “red flag” identified among the fraud cases disclosed in the survey—representing 32 percent—was “excessive control or unwillingness to have others cover his/her job duties,” according to the results. In fact, 47 percent of the cases weren’t discovered until another person performed the perpetrator’s duties for one reason or another.

The second-highest red flag was “repeated lying or deception,” followed by “family problems,” “living beyond his/her means,” and “other moral or spiritual failures.”

Lower on the list were “medical issues in family,” “expressed lack of job satisfaction,” and “loss of spouse’s job.”

When asked about red flags, a sizable portion of respondents selected “Other.” Asked to clarify, the bulk of the respondents said there either were no red flags, the person wasn’t caught and the fraud was later detected, or the red flags weren’t exhibited within the church and only learned of later.

In his comments about red flags, Dimos noted the “fraud triangle”—the illustration often used to describe financial misconduct. It forms a triangle with these three points: pressure (or incentive), rationalization, and opportunity.

“As church leaders, we can’t control what financial pressure someone may experience, like a family medical issue, nor can we stop people from rationalizing that it is okay to steal from the church,” he said. “But church leaders can create processes that prevent someone from having the opportunity to abuse funds.”

Red flags are consistent in other sectors

Interestingly, Church Law & Tax’s survey results closely tracked with the 2020 Report to the Nations by the Association of Certified Fraud Examiners (ACFE), Salsbery said. In particular, with greater positions of authority and tenure came greater degrees of losses for the organizations, he added.

The ACFE report showed the median losses for employee-caused fraud measured $21,000, then jumped to $95,000 for managers and supervisors, and $250,000 for executive-level positions.

“This correlation of higher fraud losses for long-tenured, experienced leaders makes sense. Given their influential leadership roles, they usually have more access to the assets of the church and have had that access for a long time,” Salsbery said. “The first two questions I ask ministries when I conduct [fraud investigations] is: (1) How long was the person in the role? and (2) What access did they have to bank accounts, other assets, and financial activities of the church during that time?”

Given the frequency and consistency of the red flags, whether in secular settings or church settings, leaders are actually positioned well to help protect their churches, noted Vonna Laue, a CPA and senior editorial advisor for Church Law & Tax who co-led the survey project.

“The red flags have not changed over the years in any study you review, and they are the same across entities from churches to Fortune 500 companies,” Laue said.

Leaders need “an awareness of the red flags,” she added, and give careful consideration when those serving in financial roles exhibit “at-risk behaviors.”

NEW! Safeguarding Your Church’s Finances—a multi-session video course for pastors, board members, staff, and volunteers on the basics of fraud prevention. LEARN MORE!

Matthew Branaugh is an attorney and editor for Church Law & Tax.

Key Tax Dates October 2021

Deadline for church employees with six-month extensions for filing 2020 tax returns.

If your church or organization reported withheld taxes of $50,000 or less during the most recent lookback period (for 2021 the lookback period is July 1, 2019, through June 30, 2020), then withheld payroll taxes are deposited monthly. Monthly deposits are due by the 15th day of the following month.

Note, however, that if withheld taxes are less than $2,500 at the end of any calendar quarter (March 31, June 30, September 30, or December 31), the church need not deposit the taxes. Instead, it can pay the total withheld taxes directly to the IRS with its quarterly Form 941. Withheld taxes include federal income taxes withheld from the employee’s wages, the employee’s share of Social Security and Medicare taxes, and the employer’s share of Social Security and Medicare taxes.

Semiweekly requirements

If your church or organization reported withheld taxes of more than $50,000 during the most recent lookback period (for 2021 the lookback period is July 1, 2019, through June 30, 2020), then the withheld payroll taxes are deposited semiweekly.

This means that for paydays falling on Wednesday, Thursday, or Friday, the payroll taxes must be deposited on or by the following Wednesday. For all other paydays, the payroll taxes must be deposited on the Friday following the payday.

Note further that large employers having withheld taxes of $100,000 or more at the end of any day must deposit the taxes by the next banking day. The deposit days are based on the timing of the employer’s payroll. Withheld taxes include federal income taxes withheld from the employee’s wages, the employee’s share of Social Security and Medicare taxes, and the employer’s share of Social Security and Medicare taxes.

October 15, 2021: Tax returns due for church employees with extensions

Last day to file a 2020 federal income tax return for taxpayers who obtained an automatic six-month extension by filing a Form 4868 by April 15, 2021.

Richard R. Hammar is an attorney, CPA and author specializing in legal and tax issues for churches and clergy.

A zoning board sought to shut down City Walk Urban Mission in Tallahassee, Florida, through the enforcement of zoning code. This video case study shows how Pastor Renee Miller, the executive director of City Walk, worked with attorney Noel Sterett to successfully navigate the issue and continue the ministry’s work in Tallahassee.

Church Law & Tax members can watch the full Religious Land Use & the Church: Virtual Roundtable series, which includes an insightful discussion with leading attorneys, a companion PDF guide, and another video case study featuring a church that faced government challenges to a property it planned to purchase.

Matthew Branaugh is an attorney and editor for Church Law & Tax.

Religious Land Use & The Church: A Virtual Roundtable

A virtual roundtable of attorneys discusses an often overlooked religious land use law.

Featuring attorneys Midgett Parker, John Mauck, Noel Sterrett, Eric Treene, and Matthew Branaugh

The Religious Land Use and Institutionalized Persons Act (RLUIPA) was passed unanimously in 2000 by the US Congress and signed into law by President Bill Clinton. But nearly 25 years later, many church leaders remain unaware of how this law can help them avoid—or at least navigate—challenges posed by governments, agencies, and associations regarding the purchase or use of property for worship and other religious purposes.

This virtual roundtable, featuring attorneys Midgett Parker, John Mauck, Noel Sterrett, and Eric Treene, explores why every church should understand the ins and outs of this valuable law, even if your congregation has yet to experience any obstacles from local government or zoning officials or neighborhood associations. It is conveniently set up in five segments for church leaders to watch either individually or as a board, committee, or leadership team.

In addition, Matthew Branaugh, an attorney and editor for Church Law & Tax, shares two video case studies regarding how RLUIPA helped two pastors successfully overcome obstacles presented by their local officials.

To get the most out of the roundtable, we suggest you download this PDF. It will help guide you through the video series and offer helpful notes and highlights for future reference.

If your church references Robert’s Rules of Order Newly Revised in its bylaws—or uses it by tradition—it’s important to know that the 12th edition, released in late 2020, is now the current authority. This edition contains more than 89 substantive changes, and if your bylaws don’t specify an edition, the 12th edition now applies automatically.

Why This Matters

Most church bylaws that name Robert’s Rules automatically default to the latest edition. If your bylaws specify an older edition, such as the 7th (1970), you must use that version unless you amend your bylaws to state “the current edition.”

Key Point: If your church uses Robert’s Rules but hasn’t reviewed the updates in the 12th edition, now is the time.

Other Parliamentary Authorities

While Robert’s Rules is the most common, other worthy options exist.

What’s New in the 12th Edition?

Below are 17 significant changes church leaders should understand.

1. Motion to Lay on the Table

Cannot be used to kill debate.

Should only be used to set aside discussion temporarily for urgent matters.

Use “Postpone Indefinitely” to permanently end debate.

2. Vice President’s Role Clarified

Vice presidents act only when the president is absent.

Cannot appoint committees if the bylaws assign that to the president.

In succession cases, the VP becomes president unless bylaws state otherwise.

3. Executive Sessions

Discussions in executive session are secret.

Actions taken can be disclosed only as needed to implement them.

Assemblies may vote to release more info by amending previously adopted actions.

4. Electronic Voting

Secret ballots can be conducted using electronic keypads.

Write-in options and independent tallies are required for elections.

5. Board Minutes Access

Normally, only board members may view minutes.

Assemblies can vote to release minutes with a two-thirds vote or majority vote with notice.

6. Terms of Office

Actual terms may vary depending on meeting dates.

Bylaws should specify start and end points clearly.

7. Bylaw Revisions Must Be Authorized

Only a properly authorized committee can draft a full bylaw revision.

Critical Distinctions: Bylaws vs. Robert’s Rules

Robert’s Rules has increasingly addressed church governance areas better left to:

Church charters

Bylaws

Denominational documents

Nonprofit corporation laws

Rule 1: Church bylaws always override Robert’s Rules.

Rule 2: If Robert’s Rules covers non-parliamentary topics, those provisions are secondary to governing documents.

Examples:

If bylaws state a 20% quorum, and state law says 10%, use the bylaws.

The sequence of articles in your bylaws does not need to matchRobert’s Rules.

Additional Key Updates from the 12th Edition

8. Sample Rules for Electronic Meetings

Includes templates for various formats: internet, phone, hybrid.

Legal review is advised before adoption.

9. Excluding Nonmembers from Meetings

Assemblies can exclude nonmembers by a majority vote without entering executive session.

10. Ratifying Invalid Meetings

Actions taken at unauthorized meetings can be ratified.

Example: Online meeting held without bylaw approval can be validated post hoc.

11. Changing Ballots

Votes taken by secret ballot cannot be changed after submission.

12. Secrecy of Ballots

Ballot voting requirements cannot be suspended, even by unanimous vote.

13. Secret Ballots = Ballots

Clarifies that all ballots are considered secret by definition.

14. Ballot Voting by Mail

Bylaws should address tie-breaking procedures.

15. Ex Officio Officers

If not under the organization’s authority, they can vote but aren’t counted in quorum.

If they are officers, they must participate and count toward quorum.

16. Receiving Reports

No motion needed to “receive” a report.

Reports without recommendations can be filed.

Accepting a report = endorsing it fully.

17. Notice of Bylaw Amendments

Bylaws should specify deadlines for notice and delivery of amendment text.

If a conflict arises (e.g., quorum size or officer removal), always defer to the highest-ranked authority relevant to the issue.

Caution: If your bylaws or state law already cover an issue (like discipline or quorum), Robert’s Rules is not controlling.

Bottom Line for Church Leaders

Before adopting the 12th edition of Robert’s Rules—or assuming it applies—review your bylaws and understand what governs your church. If needed, seek legal counsel.

Additional Reading

Attorney Sarah Merkle, a professional registered parliamentarian and senior editorial adviser for Church Law & Tax, wrote a five-part series, “Mastering Meeting Basics,” which dives deeper into planning and leading church business meetings. She also authored a companion four-part series detailing a hypothetical case study that applies the rules and principles.

We’ve used a combination of AI and human review to make this content easier to read and understand.

Richard R. Hammar is an attorney, CPA and author specializing in legal and tax issues for churches and clergy.

Editor’s Note. This video is part of the Advantage Membership. Learn more on how to become an Advantage Member or upgrade your membership.

Churches today face an unprecedented number of employment-related issues, thanks to evolving state and federal laws and court decisions. Church leaders understandably wrestle with numerous questions as result, whether about the ministerial exception, discrimination laws, FLSA—and more.

Attorney and CPA Frank Sommerville, a Church Law & Tax Senior Editorial Advisor, recently published an article series covering ministerial exception, job descriptions, employee handbooks, and internships for ChurchLawAndTax.com. Now, in this one-hour webinar for Church Law & Tax, Sommerville provides his more than 30 years of legal and accounting expertise just for Advantage Members and their employment-related questions.

This exclusive webinar will help you and your pastors, executive pastors, HR directors, business administrators, and board members address any uncertainties, concerns, and ambiguities you face with employment matters.

If your church or organization reported withheld taxes of $50,000 or less during the most recent lookback period (for 2021 the lookback period is July 1, 2019, through June 30, 2020), then withheld payroll taxes are deposited monthly. Monthly deposits are due by the 15th day of the following month.

Note, however, that if withheld taxes are less than $2,500 at the end of any calendar quarter (March 31, June 30, September 30, or December 31), the church need not deposit the taxes. Instead, it can pay the total withheld taxes directly to the IRS with its quarterly Form 941. Withheld taxes include federal income taxes withheld from employee wages, the employee’s share of Social Security and Medicare taxes, and the employer’s share of Social Security and Medicare taxes.

Semiweekly requirements

If your church or organization reported withheld taxes of more than $50,000 during the most recent lookback period (for 2021 the lookback period is July 1, 2019, through June 30, 2020), then the withheld payroll taxes are deposited semiweekly.

This means that for paydays falling on Wednesday, Thursday, or Friday, the payroll taxes must be deposited on or by the following Wednesday. For all other paydays, the payroll taxes must be deposited on the Friday following the payday.

Note further that large employers having withheld taxes of $100,000 or more at the end of any day must deposit the taxes by the next banking day. The deposit days are based on the timing of the employer’s payroll. Withheld taxes include federal income taxes withheld from employee wages, the employee’s share of Social Security and Medicare taxes, and the employer’s share of Social Security and Medicare taxes.

September 15, 2021: Quarterly estimated tax payments for certain employees and churches

Filing for certain ministers and self-employed workers

Ministers (who have not elected voluntary withholding) and self-employed workers must file their third quarterly estimated federal tax payment for 2021 by this date. A similar rule applies in many states to payments of estimated state taxes.

Nonminister employees of churches that filed a timely Form 8274 (waiving the church’s obligation to withhold and pay FICA taxes) are treated as self-employed for Social Security, and as a result are subject to the estimated tax deadlines with respect to their self-employment (Social Security) taxes unless they ask their employing church to withhold an additional amount of income taxes from each paycheck that will be sufficient to cover self-employment taxes (use a new Form W-4 to make this request).

Payments for unrelated business income tax liability

A church must make quarterly estimated tax payments if it expects an unrelated business income tax liability for the year to be $500 or more. Use IRS Form 990-W to figure your estimated taxes. Quarterly estimated tax payments of one-fourth of the total tax liability are due by April 15, June 15, September 15, and December 15, 2021, for churches on a calendar-year basis. Deposit quarterly tax payments electronically using the Electronic Federal Tax Payment System (EFTPS).

Richard R. Hammar is an attorney, CPA and author specializing in legal and tax issues for churches and clergy.

Image: AdobeStock/ Irina

Part 3 of 6

Internships: Blessings or Blind Spots?

Explore the essential guide to church internship programs, covering legal compliance, FLSA rules, risk management, and strategies for training future church leaders while protecting your ministry.

This series of articles on church employment aims to help give clarity, offer best practices, and encourage tax and labor law compliance in several key areas of church employment:

Part 1Applying the Ministerial Exception to Church Employees

Part 2 Developing Strong Job Descriptions for Employees and Volunteers

Part 3 Internships: Blessings or Blind Spots?

Part 4 The Importance of a Legally Sound Employee Handbook

Many churches believe that part of their mission is to train the next generation of ministers and lay leaders. While Bible schools and seminaries provide information and knowledge, most individuals need hands-on experience to apply what they have learned.

In a tradition that goes back to Joshua serving and learning from Moses, churches open their doors to qualified individuals seeking hands-on experience. Churches frequently use the term “intern” to describe these workers.

Interns benefit from the work experience, résumé enhancement, career exploration, networking opportunities, and, sometimes, the potential for a job offer from the church. Unfortunately, the term “intern” does not have a statutory definition, so each church defines the term to suit its purposes. While the meaning of “intern” varies among churches, churches often believe that using the term allows them to escape all employment rules.

Note. For purposes of this article, the term “intern” means temporary workers serving the church as part of either formal or informal training to prepare for future service to a local church.

In addition to frequently failing to apply employment laws to interns, churches frequently fail to recognize the risks associated with interns. This article guides churches regarding the regulatory and risk environments for their internship programs, assisting them in constructing legally compliant internship programs, and avoiding common risks.

Applying employment laws to interns

The Fair Labor Standards Act (FLSA) imposes minimum wage and overtime requirements on qualifying employers and employees. While attorneys and law professors debate its application to churches, my experience is that most churches qualify as employers under the FLSA.

If a church does not qualify as an employer under the FLSA, individual employees at a church can still be covered by the FLSA. If FLSA does not cover either the church or the employee, then many state employment laws impose similar minimum wage and overtime rules on the relationship between the church and its employees. In any event, the church must consider the employment laws that apply to its relationships with interns.

Also, see the FLSA page from the US Department of Labor (DOL). Consult an employment lawyer or a human resources professional before making decisions about the application of the FLSA to interns and other employees.

Volunteer versus employee

No employment law applies to volunteers. Many churches consider their internship programs to be “volunteer” programs without genuinely understanding the term “volunteer.” As a result, some interns qualify as “volunteers” while many interns fail the volunteer test.

In this context, the volunteer test means the individual receives no compensation, expenses, or benefits from the church and volunteers his or her services solely for humanitarian or religious purposes.

The ban on compensation includes noncash compensation, such as housing, food allowances, and so on. If the church provides compensation (cash, scholarships, stipends, or noncash expenses, such as housing or gas), the worker does not qualify as a volunteer, and employment laws likely apply to that relationship.

FLSA and interns

Before reviewing the application of employment laws to interns, it is necessary to remember that no employment laws apply to workers classified under the ministerial exception. Therefore, it is essential, as with any other worker, to first evaluate the application of the ministerial exception to the intern position. If an intern receives compensation but qualifies for the ministerial exception, then the FLSA or state law equivalent does not apply to that intern.

Every intern that receives compensation and is not subject to the ministerial exception is likely an employee under either the FLSA or applicable state law despite common misconceptions held by many churches.

Defining who is an ‘intern’ under FLSA

The DOL has applied the FLSA to some interns since its inception in 1938, resulting in a US Supreme Court decision in 1947 (Walling v. Portland Terminal Co., 330 U.S. 148). The definition of an intern has evolved since then, especially as applied to interns in for-profit settings. Still, there are implications for churches and other nonprofits.

Consider, specifically, the DOL’s Fact Sheet #71, Internship Programs Under The Fair Labor Standards Act. It states that the DOL will apply a “primary beneficiary” analysis to determine the application of the FLSA to unpaid interns. It then lists seven factors that the DOL will consider the extent to which:

The intern and the employer clearly understand that there is no expectation of compensation. Any promise of compensation, express or implied, suggests that the intern is an employee—and vice versa (emphasis added).

The internship provides training that would be similar to that which would be given in an educational environment, including the clinical and other hands-on training provided by educational institutions.

The intern’s formal education program is tied to the internship by integrated coursework or the receipt of academic credit.

The intern’s academic commitments and academic calendar are accommodated by the internship.

The internship’s duration is limited to the period in which the internship provides the intern with beneficial learning.

The intern’s work complements, rather than displaces, the work of paid employees while providing significant educational benefits to the intern.

The intern and the employer understand that the internship is conducted without entitlement to a paid job after the internship.

Fact Sheet footnote

The DOL Fact Sheet then states in a footnote: “Unpaid internships for public sector and nonprofit charitable organizations, where the intern volunteers without expectation of compensation, are generally permissible.” Therefore, if interns receive no compensation, they may work at the church as volunteers. The FLSA will not apply even if the above DOL criteria are not fully implemented into the program.

Once the church provides any compensation (cash or noncash, actual or implied), the FLSA likely applies to the position, regardless of whether or not the compensation triggers tax consequences. Unless the ministerial exception applies, it is unlikely interns can be classified as “exempt” employees because they are typically paid less than the minimum salary requirement of $684 per week. So, the church must pay minimum wage and overtime to compensated interns.

Note. Twenty-nine states have set a higher minimum wage than the federal minimum wage. Also, California measures overtime on a daily basis.

The FLSA allows a lower minimum wage for certain qualified newly hired employees under the age of 20. This lower minimum wage applies only to the first 90 days of employment to allow for training. This lower minimum wage has many additional requirements, including that the younger worker cannot replace a regular worker. Unless the church specifically designed its internship program to meet the requirements of the lower minimum wage with the assistance of an employment attorney, this lower minimum wage will not apply to interns.

Calculating intern pay when the FLSA applies

Since interns are generally nonexempt, churches must require interns to keep timesheets because they need to prove interns are paid at least minimum wage.

Churches may pay a flat weekly amount (salary) as long as the timesheets show that the weekly amount meets or exceeds minimum wage, and that any overtime is paid if earned. Under the salary model, the salary cannot be reduced if the intern works less than 40 hours, and the church must pay overtime for all hours over 40.

Consider, for example, that an intern receives $400 per week. If the intern works 40 hours that week, the intern received at least the federal minimum wage.

But if the intern worked 60 hours, the intern has not received minimum wage ($6.15 per hour instead of $7.25 per hour). In that case, the church must increase the weekly amount to $435 (60 times $7.25). Now the church must add overtime compensation.

Two potential methods exist:

Method 1: 20 hours x $10.875 (1.5 x $7.25 x 20 hours) = $217.60. Under Method 1, the intern receives $435 + $217.60 = $652.60.

Method 2 (only applies if the salary model applies): 20 hours x $3.625 (.5 x $7.25) = $72.50. Under Method 2, the intern receives $435 + $72.50 = $507.50.

The DOL more thoroughly explains this calculation in Fact Sheet #82, Fluctuating Workweek Method of Computing Overtime Under the Fair Labor Standards Act (FLSA)/“Bonus Rule” Final Rule.

State labor laws

No discussion on interns is complete without considering state labor laws. Forty-five states have minimum wage laws. (Alabama, Louisiana, Mississippi, South Carolina, and Tennessee do not have state minimum wage laws as of August of 2021.)

If a church believes that the FLSA does not apply to it, that church still must comply with state labor laws. If its internship program meets the state definition of a training program and the intern qualifies for a lower minimum wage because they are less than 20 years of age, the church may pay qualifying interns a reduced minimum wage.

Consult an attorney

As noted above, many states have modified or eliminated this lower minimum wage program. Churches should confirm all the state and local minimum wage requirements before implementing an internship program at this lower minimum wage. The church should also work with a local employment attorney to design the internship program to meet the local, state, and federal requirements.

Further, all states have enacted a version of a payday law to protect employees from employers who may not always pay them what they are owed.

Additional Reading: Attorney Richard Hammar analyzes notable court decisionsabout common employment disputes.

These payday laws govern how frequently employees must be paid. For example, some churches only pay the intern at the end of the internship to encourage them to complete the internship term. But such practices violate state payday laws.

The mandatory maximum payday frequency ranges from one week to one month.

Here is a chart of maximum payday frequency maintained by the DOL.

Caution. There are penalties for violating payday laws, and the penalties can be stiff. For example, the Texas Payday Law imposes a $1,000 penalty for each violation.

Example. An internship lasts eight weeks. In Texas, since the intern is nonexempt, the payday law requires payment semimonthly. If the church paid a lump sum at the end of eight weeks, it would be subject to a penalty for each failure to pay the intern semimonthly during the eight weeks. Since only the last payday was timely, the church could owe up to a $1,000 penalty for each of three prior paydays.

Payday laws also prevent employers from deducting unauthorized amounts from an employee’s pay. Churches cannot deduct any amount other than payroll taxes from an employee’s pay without their specific written permission.

Payday law penalties apply if the church deducts anything other than payroll taxes from an intern’s paycheck without the intern’s written authorization, even if the church maintains a separate policy that requires the deduction from workers’ pay for amounts owed to the church.

Compensable Time Calculations

Churches must compensate non-volunteer and nonministerial exception interns for all time worked and on standby as defined by the FLSA because they are nonexempt. As mentioned earlier, all non-volunteer and nonministerial exception interns must maintain timesheets and provide them to the church.

The FLSA allows the employer to select the minimum time increment to measure time worked and/or on standby. Time can be measured in increments of a tenth of an hour (6 minutes) up to a maximum of a one-quarter hour (or 15 minutes).

Time worked and/or on standby

If interns subject to minimum wage laws show up early and sit at their desks, they begin accruing time paid for work when they sat at their desks. It does not matter if they were working or not. The same rule applies at lunchtime (see below) and if they linger after their shift ended.

If the church does not want to pay interns who report early or stay late, it should provide a breakroom for interns to use and not owe them pay for that time.

What about the compensation rules for off-duty calls, emails, and texts? In determining whether time spent responding to such communications is compensable, the factors that courts have considered include:

the average number of calls, texts, or emails the employee responds to during the off-duty period;

the required response time: in other words, how quickly the employee must respond and the amount of time spent responding;

whether an employee is subject to discipline for missing or being late to a call-back;

the extent to which an employee can engage in other activities while on-call; and

the nature of the employee’s occupation (in some jobs, it is the nature of the job to be paid to be available to respond immediately to a situation).

Some states require employers to pay a minimum amount of time for each off-duty call, email, or text where the person responded during off-duty time.

Travel

Business travel during a typical workday is compensable. Travel on weekends is compensable if during the typical weekday work hours.

Training

All training related to the employer is compensable.

Breaks, lunch, retreats, and camps

Breaks less than 20 minutes are compensable. Lunches of 30 minutes or more are not compensable. If the intern is on-duty 24 hours straight, then mealtimes and sleep are compensable.

Note. Some states have mandatory breaks and lunchtimes that must be compensated.

Employers who require interns to remain on the employer’s premises and to respond to calls and interruptions during an intern’s meal periods and sleep time are required, in most circumstances, to pay the interns for their meal periods and sleep time.

Retreats and camps present challenges to compensating interns. Frequently, the intern is required to be on duty 24 hours a day during the retreat or camp. Under the usual FLSA rules, the intern must be paid for 24 hours a day.

However, a church can avoid paying for on-duty sleep periods only if it has an express or implied agreement to exclude such periods from work time, the church has furnished adequate sleeping facilities, and the intern’s workday is 24 hours or longer.

Caution. Under no circumstances may a church avoid paying for on-duty sleep time if the intern has not had the opportunity to receive five or more hours of uninterrupted sleep. Finally, under no circumstances can a church exclude more than 8 hours of on-duty sleep time per 24-hour shift when computing an intern’s overtime pay. Some states have additional rules for camp workers that may apply to interns as well.

Tax Issues

If the intern receives compensation in any form, it is taxable unless a specific Internal Revenue Code section excludes the item from taxation.

The Internal Revenue Code, Section 119, excludes from taxation employer-provided meals and housing if (1) the employee must live in the housing and accept the meals as a condition of employment, (2) the housing or meals are located on the business premises of the employer, and (3) the meals that are provided must be required for the convenience of the employer.

A church cannot exclude the value of meals or housing from the intern’s taxable income unless it meets Section 119 requirements.

Example. A church rented an off-campus apartment for two interns during its program. Since the apartment rent does not qualify for exclusion under Section 119, the apartment cost must be split two ways and included in both interns’ taxable income.

Business expenses that are paid or reimbursed under a qualifying accountable expense reimbursement plan are excluded from taxable income. Intern meals and lodging cannot be reimbursed under a qualifying accountable business expense plan unless the expense would also be allowed for other church employees. For example, if an intern rented an apartment, the reimbursement of the cost of the apartment is added to the intern’s taxable compensation. On the other hand, if an intern conducted a Bible study with several students and bought pizza for them, then the pizza cost can be reimbursed tax free.

If an intern has received a ministerial credential (ordained, licensed, or commissioned) from a church, and the intern performs ministerial duties, a church may designate part of the intern’s compensation as a housing allowance under Section 107 of the tax code.

Note. If an intern qualifies as a minister for federal tax purposes, the church is also prohibited from withholding payroll taxes from that intern.

Craft job descriptions for all interns

Churches should have written job descriptions for interns. These written instructions help guide the church and the intern regarding expectations.

If the internship is for ministerial students, the church should draft a job description to qualify for the ministerial exception. If the internship involves nonministerial students, the church should consider structuring the program as a volunteer program to avoid employment compliance issues.

Again, though, even unpaid interns should have a job description detailing his or her responsibilities.

A Plan for Minimizing Risk

Unfortunately, the rigorous hiring and training processes utilized for other church employees are not always applied to interns. Yet, the church must proactively protect vulnerable youth and children from harm, and such protective measures with screening and selection should not be ignored for internship programs. In fact, interns can represent a significant risk to the church.

Protecting vulnerable populations requires a church committed to proper screening, selection, and supervision of pastors, ministry leaders, and volunteers—not just interns.

Learn more about how to do this with attorney and senior editor Richard Hammar’s 14-step plan for minimizing the risk of child and youth abuse in churches.

Churches should also utilize the other youth and child resources at Church Law & Tax to minimize this risk. Misconduct by a single intern in one summer can cost the church millions of dollars, cause the loss of members, and injure individuals that will carry serious emotional scars for life.

An opportunity to train

On the flipside, an internship provides an excellent opportunity to train the next generation about safely ministering in the real world and understanding the importance of protecting vulnerable populations.

Screening candidates, following up on references, and consistently enforcing policies and procedures can help mitigate risks.

Churches must screen interns with the same careful vetting process they use for potential employees. If the intern will work in the youth or children’s ministries, he or she should go through the same process used for any youth or children’s workers.

Reference checks for minors

Churches are hampered in using background checks because most interns are young and have little or no criminal history due to their ages, or such records are sealed as juvenile offenses. Reference checks and personal interviews will become the church’s primary screening tools.

For interns who will work in youth or children’s ministries, churches ideally should request references from youth-serving institutions where the prospective interns previously served. As attorney Richard Hammar, the senior editor for Church Law & Tax, notes, “The key question to ask is whether the institution is aware of any information indicating that the applicant poses a risk of harm to minors or is in any other respect not suitable for youth or children’s ministry.”

Churches also should request the names and contact information for the prospective intern’s current pastor, as well as his or her former pastors. If candidates do not list their former pastors as references, the church should still contact those pastors.

If a reference or former pastor refuses to respond to requests for a conversation about the candidate, the candidate should be rejected.

The church should include both men and women as reference interviewers to add their perspectives and impressions about the candidates.

Enforce policies and rules

In addition to the screening process, churches need policies and processes to protect vulnerable populations from interns who engage in risky behavior.

All church safety policies should be applied to interns. Since this is likely one of the intern’s first professional ministry experiences, the church must educate the interns about the church’s policies.

The church should actively take steps to make sure the rules are followed. Interns must understand that any violation will end the intern’s participation in the program.

Policies and rules regarding relationships and contact with children and youth should be strictly enforced. The church should prohibit interns from becoming involved romantically with any youth during their term at the church.

As a risk management tool, interns working with youth should be at least five years older than those in their ministry group. The church’s policy should prohibit interns from engaging in any one-on-one visits with children or teens that are not held in public areas on the church’s premises.

Phone calls, texting, and emails

Additionally, phone calls, texting, and emails with children and youth should not be allowed unless another adult (such as the child’s parent or youth pastor) is included in the communication.

Nearly all interns will use their personal cellphones to conduct church business during their internship. But cellphones present a frequent tool for grooming children and youth for harm.

Due to the risks arising from cellphone use, the church should notify intern applicants that the church may want to check their cellphones for inappropriate interactions with children and youth during their internships. Further, the intern could be told that the church requires its interns to submit their cellphones for surprise inspections by the church’s information technology (IT) department. (The church would keep all data from the phone unrelated to church business confidential.) The applicant should sign a written consent to the search as a condition of admission into the internship. If the applicant objects, the church may want to decline to invite that applicant.

Some churches require interns to submit a weekly written report of their interactions with their ministry groups outside of formal church events. The interns also should affirm weekly, in writing, that they have followed all policies and procedures required by the church.

Note. Not only should the interns be familiar with these rules, but parents and youth must also be familiar with these rules. No matter whether the church is addressing volunteers, employees, or interns, it is vital that the church educate parents, teens, and children about these rules and the grooming tactics predators use to gain the trust of victims and their families. Parents and youth must understand the importance of the rules in protecting everyone’s safety.

Additionally, the church should provide an easy way for parents and youth to easily report rule violations to church leaders.

Training future leaders

Internship programs provide valuable avenues for training the next generation of ministers and Christian leaders. However, as beneficial as these programs can be, incorrectly administered programs can also create substantial unforeseen liabilities.

The goal is to create internship programs that are either exempt from all employment laws or comply with all the employment and tax laws. It’s also essential that rules and policies are enforced that mitigate the risks noted above.

With careful planning, an internship program can provide meaningful assistance to training the next generation of ministers and future church leaders. It also provides the church with an excellent avenue of ministry.

Thanks to CPA Elaine Sommerville for her useful comments and edits to this article.