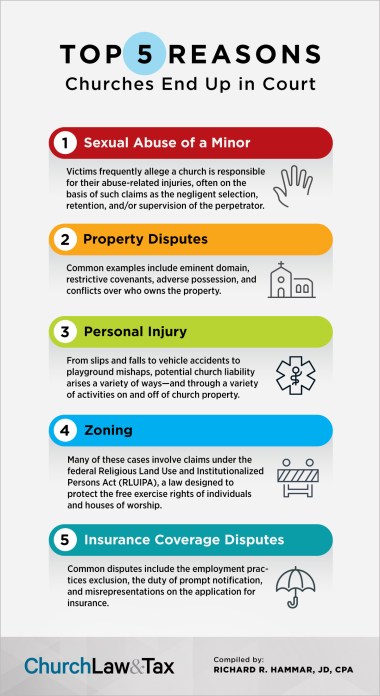

The Top 5 Reasons Churches and Religious Organizations End Up in Court

And how you can make sure your church isn’t one of the statistics.

The Editors

Since the early 1980s, attorney and CPA Richard Hammar, the cofounder and senior editor of Church Law & Tax, has read thousands of cases involving churches, religious organizations, and educational institutions.

When he does, he determines the relevance of the cases to local congregations. Many of these court decisions become the basis of articles and Legal Developments he writes for church leaders. Along with this work, he has also carefully categorized all of the court decisions—whether he writes about them or not—primarily in an effort to discern broader unfolding legal trends affecting churches.

Identifying these patterns provides a powerful point of information: by categorizing the top legal threats and then publishing about them in an understandable way, Hammar believes church leaders are better equipped to talk about potential challenges they face and how they can take action.

Through this long-standing work, it is now possible to authoritatively identify the Top 5 legal issues most likely to generate litigation targeting churches and religious organizations.

The infographic included with this article summarizes the Top 5, based on Hammar’s many years of research, providing a quick, user-friendly way to help leaders understand the trends, discuss them with staff and board members, and prioritize the efforts necessary to minimize potential pitfalls. (Download a PDF of the infographic to share with your team.)

Fortunately, church leaders can take an active role to minimize potential problems and decrease the chances of ending up in court.

One good first step is to read the articles and collections of articles listed with the Top 5 reasons described below. Another good step is to share this infographic with fellow leaders and use it as a launching point for discussions and planning.

Make child safety a priority

More than 25 years ago, Hammar was one of the first people in the country to address the growing threat of child abuse in churches. Regrettably, the threat has been—and remains—the number one reason churches end up in court each year. In response, Hammar developed Reducing the Risk: A Child Sexual Abuse Awareness Training Program.

Along with Reducing the Risk, any church of any size can get a comprehensive view of the problem, and the solutions needed to combat it, through Hammar’s 14-step plan outlined in his article “Minimizing the Risks of Child Molestation in Churches.”

Know who owns the church’s property—and what can be done with it

Property disputes often lead to litigation, whether between a church and a denomination, a church and a municipality, a church and a private party—or even a church and its own congregants. These conflicts most often involve disputes over ownership, covenants, eminent domain, or adverse possession.

Chapter 7 of Hammar’s Pastor, Church, & Law offers insights into these types of property disputes and how courts have responded over the years.

Dealing with everyday dangers

Personal injuries are another common source of litigation for churches each year. A case is usually brought by a person who alleges that he or she was injured either while visiting church property, participating in a church-sanctioned activity, or both. Common examples of claims include unsafe conditions on church property, the negligent operation of a vehicle in the course of church business, or the inadequate supervision of a church activity that results in an injury.

The injured party brings a lawsuit in the civil courts. The party must prove several elements in order to win, but the legal standard required for a party to prevail is not as difficult as the one used in criminal trials. This makes personal injury cases a particular source of trouble for churches.

Generally speaking, even if a church is found liable in a personal injury case, board members and staff members are not also personally liable. However, personal liability can arise under certain circumstances. Chapter 6 of Hammar’s Pastor, Church & Law further explains personal injuries and the potential resulting liability for a church, its board members, and its staff members.

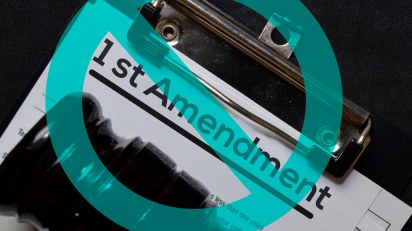

Don’t get zoned out

Municipalities, such as cities, towns, and counties, are authorized by their state governments to set zoning laws that dictate the types of buildings (and building uses) allowed in specific geographic areas. Disputes involving churches frequently arise in two ways: one, when a church located in a residential area conducts activities potentially in conflict with neighboring homeowners; or two, when churches wish to occupy or construct a building in a commercial zone that the municipality prefers to preserve for a business and the tax-generating activities it produces.

The First Amendment of the US Constitution and similar provisions in state constitutions provide protections for churches when these types of conflicts arise. Similarly, the Religious Land Use and Institutionalized Persons Act (RLUIPA) offers additional protections. Hammar explains these protections further in the zoning law section of Pastor, Church & Law’s Chapter 7.

Know what’s covered by insurance—and how

Disputes between churches and insurance companies most commonly develop in one of two ways.

One way is coverage exclusions. A coverage exclusion is a loss not covered under a general liability policy. Often, additional special coverage must be obtained in advance by a church in order for a future claim to be covered by the insurer. One common issue that is not typically covered in a general liability policy is a claim alleging sexual misconduct by a church employee or volunteer.

The other way is the duty to notify. Insurance policies typically contain strict language regarding how quickly a church must notify the insurer of a possible claim, and when a church fails to do so within the prescribed timetable, the insurer can reject the claim. Leaders must read the fine print of their policies, and also should consult with their insurance agent or broker to make certain they understand deadlines for notifying (as well as the types of situations that start the clock for those deadlines).

Check out this quick overview of the types of insurance a church should consider with action items you can take today.

Image: sanjeri

Should Our Church Agree to Host a COVID-19 Vaccination Clinic?

Key legal considerations to address before offering your facility as an immunization site.

During the reign of Marcus Aurelius, in 165 A.D., a dreadful epidemic swept through the Roman Empire. An estimated one-quarter to one-third of the population died during the 15-year ordeal. Nearly a century later, a second great plague came to Rome. Bishop Dionysius described the events in Alexandria:

At the first onset of the disease, they [pagans] pushed the sufferers away and fled from their dearest, throwing them into the roads before they were dead and treated unburied corpses as dirt, hoping thereby to avert the spread and contagion of the fatal disease; but do what they might, they found it difficult to escape.

UPDATE

In July of 2021, the US Centers for Disease Control and Prevention (CDC) updated its guidance regarding masks for unvaccinated and vaccinated persons. Learn more here.

The early church made its mark during this period, caring for and nursing the sick. According to one historian, through this “miracle working” of basic nursing, Christians may have reduced the mortality in Rome by as much as two-thirds.

So, it is no surprise that as state and local officials seek help from churches during the COVID-19 pandemic, including using church properties as vaccine administration sites, congregations are again stepping forward. As churches do so, they can take advantage of certain legal immunities and take other precautions to avoid unnecessary legal liability.

“PREP” for action

In 2005, Congress enacted the Public Readiness and Emergency Preparedness (PREP) Act to legally immunize select persons against claims for loss caused by, arising out of, relating to, or resulting from the administration of covered countermeasures, such as vaccines. The Act protects select licensed health professionals who administer vaccines in accordance with standards set by the Advisory Committee on Immunization Practices (ACIP). The Act also protects those who supervise or administer a program for dispensing vaccines when in conformity with the several Declarations under the Act by the Secretary of the Department of Health and Human Services (HHS).

Compliance with the ACIP standards, Declarations, and local public health authority’s guidance is an important aspect of ensuring legal immunity for a church participating as a COVID-19 vaccination site.

Typically, this guidance identifies the persons who are prioritized for inoculation. Adhere to these priorities and avoid the temptation to prioritize others, whether or not family or church members or church leaders.

In addition, take reasonable precautions to facilitate the safe administration of the vaccine. For inoculation sites, this includes removing hazards in the right-of-way, ensuring proper lighting, adhering to US Centers for Disease Control and Prevention (CDC) protocols, and planning for emergencies, such as serious allergic reactions or other vaccination side effects.

The PREP Act applies only to covered countermeasures, such as vaccines, and has no bearing upon other countermeasures, such as social distancing, quarantining, or lockdowns. Damages that are not proximately caused by the administration of the vaccine are not covered by the Act. For instance, the Act may cover an injury sustained by a person who trips in the tent where the vaccine is administered, but not necessarily by a person who trips while heading back to her car after vaccination.

The PREP Act does not provide any immunity with respect to willful misconduct. Also, employment and other claims are not the subject of the PREP Act—just loss caused by the administration or use of the vaccine.

Additional protections

Some states have adopted additional protections against liability for health-care providers (including workers) assisting with the pandemic and, to a lesser extent, organizations that volunteer to serve as immunization sites. Churches may be able to benefit from these protections, too.

Regardless of these protections, churches should still consult with their insurer regarding coverage. Many insurers are now excluding COVID-19 from primary coverage, but some may offer supplemental COVID-19 coverage for a fee. Churches may be able to request a signed release, waiver, and indemnity (hold harmless) from any entity wishing to host a vaccination clinic on the church’s property. Bear in mind, though, that government agencies normally have sovereign immunity, meaning that there will be a statutory limitation on the value of most public indemnity.

Similarly, a church may request signed releases, waivers, and indemnities from individuals who receive vaccinations onsite. Though their enforceability is uncertain depending upon state law, releases should be:

conspicuous;

unambiguous;

exclude intentional or reckless acts; and

state the risks of vaccination and the limited remedies available to vaccine recipients under the PREP Act.

Licensed health professionals and others identified as authorized to dispense the vaccine alone should do so. Churches should insist that only such persons inoculate onsite. Malpractice risk arising from inadequate screening, warning, evaluation, inoculating, or monitoring is reduced under the PREP Act, but in an abundance of caution, leaders should consider allowing a third party (such as a local health authority) to inoculate rather than the church itself. By doing so, the church will also avoid handling and potentially compromising the vaccine.

Aiding the greater good

Service to the public generally involves risk. Consider the Christians who confronted the great plagues in Rome. Vaccinating or offering the church as a site for vaccination is no exception, but some combination of the PREP Act, state immunities, insurance, releases, waivers, and indemnities can materially limit a church’s legal liability. Consultation with legal counsel on the front end of the effort can pay dividends while the vaccination effort itself speaks to the public about the relevance of the gospel to a world in pandemic.

Dr. Nathan A. Adams IV is a partner at Holland & Knight. His practice includes representing nonprofit and religious organizations on a variety of matters, including the First Amendment, the ministerial exception, church autonomy, and board and governance issues.

Image: qingwa | Getty

Church Facility Care During Shutdowns and Limited Use

Expert tips to keep your building in good shape and ready when life returns to the new normal.

Chris Lutes

The pandemic led many churches to close their facilities or move to limited use. This has created both maintenance challenges and opportunities for those who manage the facilities, say the experts interviewed for this article.

To help those who oversee church facilities, we collected the following tips and insights for times when a building is either shutdown or not in full use.

Lower Temperatures—but how low?

Every church wants to save money, and lowering the thermostat during the winter is one way to do just that.

“Our research has shown that temperatures as low as 45°F do not harm the structure or contents of buildings,” says a press release from The Interfaith Coalition on Energy (ICE). Such low temperatures are not harmful to those expensive church pipe organs, claims Andy Rudin, project coordinator for ICE, an organization that seeks to help congregations lower the cost of operating their facilities.

“We surveyed members of the Associated Pipe Organ Builders of America to find that they agree with our low temperature recommendations,” he said.

While lowering the temperatures is not a bad idea, says Pat Hart, executive director of the National Association of Church Facilities Managers (NACFM), he feels that 45 degrees would be too low for his facilities. Along with leading NACFM, Hart also manages a five-building church and Christian school in Everett, Washington.

When any of the buildings he manages are unoccupied, Hart says that “55 degrees is as low I would go.”

Keep the furnace running

Shutting off your HVAC, or turning it way down so it doesn’t periodically run, could create some serious mechanical problems.

“When you fire the furnace back up, you are going to have some significant maintenance issues,” says Hart. He explained that an HVAC is made to be used regularly; extended times when it’s not used can cause fan motors to malfunction, along with a number of other potentially costly problems.

He added that reheating the building would be a big issue—something that would consume a lot of costly energy. If someone walked into a building set at 45 degrees, he explained, they’d need to turn up the heat, forcing the HVAC to expend a lot of energy to reach a comfortable temperature.

Maintain consistent temperatures

It can become an issue if consistent temperatures aren’t maintained, cautions Tim Cool, chief solutions officer for Smart Church Solutions, an organization that assists with various areas related to facilities.

“Humidity and cold are major concerns for spaces that have delicate musical instruments,” Cool explains. “The damage wildly fluctuating space temps can do to a pipe organ or grand piano will negate the cost-benefit of keeping the set-points too low (or high) in a space that houses that type of investment.”

Overall, it’s important to remember that church buildings are conditioned spaces—depending on an HVAC system for heating and cooling.

“Facilities are designed to be conditioned spaces, and most designs assume that it will be conditioned consistently,” Cool stresses.

Avoid frozen pipes and mechanical room breakdowns

Temperatures that are set too low can also lead to frozen pipes that might burst. This could be especially problematic for poorly insulated pipes or pipes that run next to an outside wall.

“In churches heated by circulating water, the property committee should know where all the pipes are, particularly those running through unheated places, like under floors, inside walls and attics,” Rudin advises.

Churches must pay particular attention to the space dedicated to the HVAC, electrical systems, and water systems, Cool says.

“Many mechanical rooms have one or more exterior facing walls. They may not be insulated as well, and they are the entry point for many of the building’s systems,” Cool says. “In climates with below freezing temperatures for multiple days in a row, these spaces can become 15 to 25 degrees colder than the interior of the facility. Temperature-controlled space heaters may be necessary to ensure they do not become too cold.”

Consider installing remote thermostats

The ability to control your building’s thermostat remotely is a very good idea, Hart says. If there needs to be people in a particular part of your building during a shutdown or period of limited use, it’s good to be able to turn up your HVAC and then turn it down when they leave, Hart explains.

Cool of Smart Church Solutions agrees and adds, “This is also a great time to consider investing in communicating thermostats to allow for remote building environment monitoring.”

Keep an eye on your building

Even when your facilities are completely shut down, it’s essential to regularly inspect the building for any issues or potential problems.

Walk-through inspections should be conducted at least once a week for both “operational considerations” and possible “safety or security” issues, Cool recommends. He said night inspections should also be conducted in order to check to see if any lights are out or any other issues that wouldn’t be readily apparent during the day.

Cameras connected to an app are also a good way to check on your building—both inside and out.

“I have 90 cameras and I have access on my phone,” Hart says of his five-building church and school. “I’ll log on to see if it’s snowing and if I need to call a plow company. I have a camera on the roof where we’ve had some wind damage and I keep an eye on that.”

Preventive maintenance and needed repairs

Upkeep during shutdowns and times of limited use is essential, Hart stresses. “You have to have someone focusing on preventative maintenance and not just locking the doors and walking away,” he says.

Opportunities amid the challenges

While the pandemic shutdowns have created many challenges, Hart says it’s also created opportunities for taking care of tasks that are too easily neglected or impossible to do because people are almost always in your building.

Six tips that will keep your church from breaking the bank on big ticket facility fixes.

“There’s all this preventive maintenance or deferred maintenance that churches don’t do because they don’t have the time” or it’s difficult to schedule certain projects “because of church activities and events,” Hart says. “We’ve had an incredible nine months to go after things we didn’t have time to do before.”

Hart says that an unoccupied building would be a great time to upgrade to energy- and cost-efficient LED lighting. And there’s an added incentive to do so: rebates. Hart adds that many places offer rebates for switching to LED lighting.

Cool agrees that shutdowns or periods of limited use are the best times “to perform any repairs to the parking lot and exterior [or] entrances.” It also affords plenty of time for deep cleaning of carpets, flooring, restrooms, and kitchen areas, he says.

“Now is the time to declutter the facility and remove all extraneous items, clear out closets and clean out mechanical rooms,” Cool recommends. “Broken furniture should be repaired, replaced, or removed.”

As for any unmeet accessibility requirements, Cool says that “now is the time to make that happen. Have a clearly defined accessible route from the parking lot, into the facility, into a restroom, and into the worship space.”

Additionally, Cool says that “upgrading camera and access control is easier when the building is less occupied. He says that this is also a good time for “ensuring all OSHA required items are in place and up-to-date.”

Curtailing theft and vandalism

Hart cites another reason for keeping your property in good shape: churches need to give the appearance that that someone is around. Failure to keep the lawn mown or fix a broken window can open your church up to vandalism and theft.

“We have had school buses vandalized on a holiday,” Hart says. “People realized we weren’t here and our fuel lines had been cut and they’d drained our gas tank.”

Upkeep and checking on your buildings during shutdowns and times of limited use can greatly reduce the chances of having something stolen or your building vandalized, facility experts say.

“You need to maintain an appearance of activity,” Hart stresses.

Avoid costly “surprises”

“The churches I know that shutdown completely are the ones I worry about having difficulties with systems and breakdowns,” NACFM’s Hart says. “You can’t shutter your building.”

If you do, he warns, you might find some unfortunate surprises when you return—such as serious and costly water damage due to a water pipe that had burst.

But if you’re conducting regular facility inspections and doing any needed repairs, you’ll discover relatively minor issues before they become major—and costly—disasters.

Key Tax Dates February 2021

Key forms, including W-2s, 1099-NECs, Form 941s, and more, come due this month.

If your church or organization reported withheld taxes of more than $50,000 during the most recent lookback period (for 2021, the lookback period is July 1, 2019, through June 30, 2020), then the withheld payroll taxes are deposited semiweekly. This means that for paydays falling on Wednesday, Thursday, or Friday, the payroll taxes must be deposited on or by the following Wednesday. For all other paydays, the payroll taxes must be deposited on the Friday following the payday.

Note further that large employers having withheld taxes of $100,000 or more at the end of any day must deposit the taxes by the next banking day. The deposit days are based on the timing of the employer’s payroll. Withheld taxes include federal income taxes withheld from employee wages, the employee’s share of Social Security and Medicare taxes (7.65 percent of wages), and the employer’s share of Social Security and Medicare taxes (an additional 7.65 percent of employee wages).

Monthly requirements

If your church or organization reported withheld taxes of $50,000 or less during the most recent lookback period (for 2021, the lookback period is July 1, 2019, through June 30, 2020), then withheld payroll taxes are deposited monthly. Monthly deposits are due by the 15th day of the following month.

Note, however, that if withheld taxes are less than $2,500 at the end of any calendar quarter (March 31, June 30, September 30, or December 31), the church need not deposit the taxes. Instead, it can pay the total withheld taxes directly to the IRS with its quarterly Form 941. Withheld taxes include federal income taxes withheld from employee wages, the employee’s share of Social Security and Medicare taxes, and the employer’s share of Social Security and Medicare taxes.

February 1, 2021: Tax forms due

Copies of W-2s for employees

Churches must furnish Copies B, C, and 2 of Form W-2 (“wage and tax statement”) to each person who was an employee during 2020 by this date. This requirement applies to clergy who report their federal income taxes as employees rather than as self-employed, even though they are not subject to mandatory income tax (or FICA) withholding. Nonminister church employees must also receive a W-2.

Filing W-2s with the Social Security Administration

Churches must send Copy A of Forms W-2, along with Form W-3, to the Social Security Administration by this date. If you file electronically, the due date is also February 1, 2021.

Copies of 1099-NEC for self-employed persons

Churches must issue Copy B of Form 1099-NEC (“nonemployee compensation”) to any self-employed person to whom the church paid nonemployee compensation of $600 or more in 2020 by this date. This form (rather than a W-2) should be provided to clergy who report their federal income taxes as self-employed, since the Tax Court and the IRS have both ruled that a worker who receives a W-2 rather than a 1099-NEC is presumed to be an employee rather than self-employed. Other persons to whom churches may be required to issue a Form 1099-NEC include evangelists, guest speakers, contractors, and part-time custodians.

Filing 1099-NEC and 1096 with the IRS

Churches must send Copy A of Forms 1099-NEC, along with Form 1096, to the IRS by this date.

Distributing 1099-INT

Churches must distribute a 2020 1099-INT form to any person paid $600 or more in interest during 2020 by this date (a $10 rule applies in some cases).

February 10, 2021: Employer’s quarterly federal tax return due

Churches having nonminister employees (or one or more ministers who report their federal income taxes as employees and who have elected voluntary withholding) may file their employer’s quarterly federal tax return (Form 941) by this date instead of February 1 if all taxes for the fourth calendar quarter (of 2020) have been deposited in full and on time.

February 28, 2021: IRS forms due

Filing IRS 1098-C for reporting vehicle sale or donation

Churches file Copy A of Form 1098-C with the IRS by this date to report the sale or use of a donated vehicle. Generally, you must furnish Copies B and C of this form to the donor no later than 30 days after the date of sale if box 4a is checked, or 30 days after the date of the contribution if box 5a or 5b is checked. If box 7 is checked, do not file Copy A with the IRS and do not furnish Copy B to the donor. You may furnish Copy C to the donor. The donor is required to obtain Copy C or a similar acknowledgment by the earlier of the due date (including extensions) of the donor’s income tax return for the year of the contribution or the date that the return is filed. If filing electronically, this form is due by March 31, 2021.

Filing 1095-C and 1094-C for applicable large employers and ACA compliance

Applicable large employers, generally employers with 50 or more full-time employees (including full-time equivalent employees) in the previous year, must file a Form 1095-C for each employee who was a full-time employee of the employer for any month of the previous calendar year by this date. Generally, the employer is required to furnish a copy of Form 1095-C (or a substitute form) to the employee.

The employer also files a Form 1094-C transmittal form with the IRS (including copies of each Form 1095-C). The purpose of this form is to ensure that applicable large employers are complying with the shared responsibility provisions of the ACA. Forms 1094-C and 1095-C must be issued by March 31, 2021, if issued electronically.

Richard R. Hammar is an attorney, CPA and author specializing in legal and tax issues for churches and clergy.

Image: fizkes | Getty

Adding Emergency Provisions to Your Bylaws

How adopting these provisions allows for legally sound virtual meetings.

In 2020, the United States experienced a pandemic that shut down the country and limited physical gatherings. These lockdowns prohibited in-person meetings, including religious organization’s board and committee meetings. Churches with congregational governance could not conduct an in-person business meeting. Suddenly, the religious organization could not follow its usual governance model.

Farsighted religious organizations planned for this pandemic by including the following in their governing documents: 1) they authorized “electronic meetings”; 2) assuming the state nonprofit corporation law allows for electronic meetings, the bylaws included conference calls, video conferencing, electronic message boards, and electronic voting via the internet.

Two key emergency provisions

Churches that have not already done so would be wise to add the following two provisions to their own bylaws, to the extent allowed by their state’s law.

Meeting by electronic means

The corporation may hold a meeting by any electronic medium in which all persons participating in the meeting can speak and hear each other. The notice of a meeting by electronic means must state the meeting will be held by electronic means (including the directions to participate) and all other matters required to be included in the notice. Participation of a person in an electronic meeting constitutes the presence of that person at the meeting.

Action by consent without meeting

Any action required or permitted to be taken by the members, board of directors or committees may be taken without a meeting and with the same force and effect as an in-person meeting. Members, members of the board of directors, and committees must return the consents to the secretary. Such consent may be given individually or collectively to the secretary in writing, fax, via a secure website, or electronic mail. The action is adopted if the requisite number of consents is submitted to the secretary to approve the action, assuming all members, all directors, or committee members voted.

Emergency authorization by state statute

Frequently, state nonprofit corporation statutes authorize the religious organization to include provisions in the bylaws that become effective in an emergency. The state law will define when an emergency exists and what actions may be authorized during the emergency. A disaster declared by the President frequently allows the emergency provisions to become effective and remain effective as long as the emergency exists. Here is a sample under Texas law:

Emergency Powers. An “emergency” exists for this section if the Board of Directors’ quorum cannot readily be obtained because of some catastrophic event. If an emergency exists, the Board of Directors may: (i) modify lines of succession to accommodate the incapacity of any Director, officer, employee or agent; and (ii) relocate the principal office, designate alternative principal offices or regional office, or authorize officers to do so. During an emergency, a notice of a meeting of the Board of Directors only needs to be given to those Directors whom it is practicable, including Internet website, email, publication, or radio. One or more Corporation officers present at a meeting of the Board of Directors may be deemed Directors for the meeting, in order of rank and within the same rank and order of seniority, as necessary to achieve a quorum. Corporate action taken in good faith during an emergency binds the Corporation and may not be the basis for imposing liability on any Director, officer, employee, or agent of the Corporation on the ground that the action was not authorized. The Board of Directors may also adopt emergency bylaws, subject to amendments or repeal by the full Board of Directors, which may include provisions necessary for managing the Corporation during an emergency including; (i) procedures for calling a meeting of the Board of Directors; (ii) quorum requirements for the meeting; and (iii) designation of additional or substitute Directors. The emergency bylaws shall remain in effect during the emergency and shall be revoked after the Board of Directors has deemed that the emergency has ended.

Check to see if your state law contains such a statute.

Adopting the two provisions

Churches will need to research whether these provisions are authorized by their state’s nonprofit corporation statute. These provisions may need to be modified to fit the state law requirements. If authorized, churches will need to amend their bylaws in the manner prescribed by the existing bylaws or state nonprofit corporation statute.

For congregationally lead churches, the members usually must approve bylaws amendments in a properly noticed and called in-person meeting. For board governed churches without members, the board of directors must approve the bylaws amendments in a properly noticed and called in-person meeting.

In many states, a majority vote is required to amend the bylaws but some state laws and bylaws require a two-thirds vote to approve the bylaws amendments. If the government authorities are prohibiting in-person meetings, then the amendments will have to wait until an in-person meeting can be convened.

Frank Sommerville is a both a CPA and attorney, and a longtime Editorial Advisor for Church Law & Tax.

Image: Michael H | Getty

Temporary Relief for Valuing Personal Use of Church-Owned Automobiles

Taking advantage of this relief affects the amount reported on Form W-2.

Kaylyn Varnum, Michele Wales, and Mike Batts

On January 4, 2021, the IRS released Notice 2021-7, which provides unique and temporary flexibility regarding the valuation of employees’ personal use of employer-provided automobiles—including church-owned vehicles.

Specifically, the IRS Notice provides temporary relief for employers using the automobile lease valuation rule for 2020 by allowing employers in certain circumstances to switch to the vehicle cents-per-mile rule as of March 13, 2020. Depending upon the specific facts and circumstances surrounding employees’ personal use of a church’s automobiles, this flexibility could provide tax savings to the church and its employees for 2020.

The Notice states, in part:

As a result of the pandemic, many employers suspended business operations or implemented telework arrangements for employees. Consequently, employers have indicated that business and personal use of employer-provided automobiles has been reduced for employees. However, due to the way in which the value of an employee’s personal use of an employer-provided automobile is computed using the automobile lease valuation rule, . . . employers have noted a resulting increase in the lease value required to be included in an employee’s income for 2020 compared to prior years. In contrast, determining the value of an employee’s personal use of an employer-provided automobile using the vehicle cents-per-mile valuation rule results in income inclusion of only the value that relates to actual personal use, thereby providing a more accurate reflection of the employee’s income in these circumstances.

Taking advantage of this temporary option will affect the amount of taxable wages reported on 2020 Forms W-2 for employees who use a church-provided vehicle partially for business and partially for personal purposes. As many employers are finalizing 2020 payroll information now, we recommend that churches immediately evaluate whether they and their employees may benefit from the flexibility this notice offers.

Brief Background

If a church provides an employee with an automobile that is available to the employee for personal use, the value of the personal use must generally be included in the employee’s taxable wages and reported on Form W-2.

As further described in our whitepaper, there are several valuation rules that a church may use to calculate the value of the personal use of church-provided automobiles, including the “general valuation rule” (based on a facts and circumstances determination); the “vehicle cents-per-mile valuation rule”; the “automobile lease valuation rule”; and the “commuting valuation rule.” Historically, the automobile lease valuation rule has been the most common method used by our clients because of certain historical limitations related to the use of the commuting valuation rule and the vehicle cents-per-mile valuation rule, as well as the subjectivity of the general valuation rule.

However, in 2018, the Tax Cuts and Jobs Act (TCJA) made a change to the requirements necessary to use the vehicle cents-per-mile valuation method, making the method more widely usable. The cents-per-mile valuation rule must typically be adopted for a vehicle as of the first day on which the vehicle is used by an employee for personal use.

Additionally, federal tax regulations require that the valuation methodology chosen by an employer must be used consistently. Employers were not generally able to switch immediately to the cents-per-mile valuation method after the passage of the TCJA on vehicles for which they were already using the annual lease valuation rule. They could generally use the cents-per-mile rule with respect to new vehicles placed in service on or after January 1, 2018. (Other specific criteria apply for using the cents-per-mile valuation rule including, but not limited to, a maximum value for the automobile on the first date that it is made available to an employee for personal use. (See our whitepaper for more details.)

Potential Tax Savings

In certain situations, the vehicle cents-per-mile valuation rule may result in a lower valuation than the automobile lease valuation rule—resulting in potential tax savings for both the employer and employee. For much of 2020, in situations where employees were supplied with employer-provided automobiles that were used very little for business, the valuation of personal use under the cents-per-mile valuation method may be significantly lower. (This lower valuation may also apply for part of 2021.)

Notice 2021-7 allows an employer that has historically utilized the annual lease valuation rule to utilize the vehicle cents-per-mile valuation method for qualifying vehicles beginning March 13, 2020. (They must pro-rate the personal use value under the annual lease value method for the period from January 1, 2020 through March 12, 2020.) Employers may choose to revert back to the annual lease valuation rule for 2021 or continue using the vehicle cents-per-mile valuation method in 2021 (assuming the arrangement otherwise meets the requirements for valuation under that method). The method chosen for 2021 must generally be used for all subsequent years so long as the arrangement continues to qualify for valuation under that method.

This information was adapted from an article that originally appeared in the Batts Morrison Wales & Lee Nonprofit Special Alert e-newsletter. Used with permission.

Kaylyn Varnum, CPA, is a partner and the assistant national director for tax services at Batts Morrison Wales & Lee (BMWL); Michele Wales, CPA, is a partner and the national director for tax services at BMWL; Michael (Mike) E. Batts, CPA, is the managing partner of BMWL. BMWL is an accounting firm dedicated exclusively to serving nonprofit organizations across the United States.

Image: Kiattisak Lamchan / EyeEm | Getty

Q&A: Can Church Employees Receive Tax-Free Assistance for COVID-Related Hardships?

Section 139 of the Internal Revenue Code allows you to offer nontaxable financial help for expenses directly related to the coronavirus.

Our church’s employees have experienced extreme financial hardships because of the coronavirus pandemic. Is it possible to offer them financial assistance without having to report these “benevolent funds” on their W-2s?

A church may not provide general benevolence to employees on a tax-free basis. However, Section 139 of the Internal Revenue Code allows employers to provide disaster assistance on a tax-free basis.

In March of last year, President Trump declared the COVID-19 outbreak a national disaster. If an employer has adopted a Section 139 Disaster Relief Plan, the employer may assist its employees for unusual expenses directly related to them having COVID.

For example, the employer may pay expenses related to their COVID infection or caused by their COVID infection. Expenses could include medical expenses related to the COVID infection not covered by insurance, such as medicines. Expenses could include extra COVID cleaning supplies.

Section 139 expenses could include extra childcare expenses incurred because the employee cannot care for their children without potentially infecting them. It might include tutoring expenses because the employee cannot help with their children’s homework.

COVID affects different employees differently, but all employees infected by or exposed to the virus must quarantine. If an employee can work remotely, then Section 139 expenses might include equipping the employee with a home office, including a computer, desk, chair, office supplies, and increased internet capacity while quarantined.

Some employees become seriously ill from COVID. Section 139 expenses might include the expense of a home healthcare provider. If the employee passes away from COVID, Section 139 might include the funeral expenses.

If the employee incurs legal expenses that arise from COVID, Section 139 might cover those legal expenses, such as drafting a healthcare power of attorney.

The regulations are not clear regarding whether an infected member’s family also allows for Section 139 benefits. When in doubt, consult with a tax expert about this and any other questions regarding Section 139.

While the regulations do not require a written plan, I strongly recommend a written plan so that the church complies with all the requirements to allow for tax-free benefits. I also recommend that an application be filled out by the employee so the church can document that the employee meets the Section 139 requirements.

Frank Sommerville is a both a CPA and attorney, and a longtime Editorial Advisor for Church Law & Tax.

Image: CharlieAJA | Getty

What the New Coronavirus Stimulus Package Means for Churches

The Coronavirus Stimulus Package creates an extension of the Paycheck Protection Program with different eligibility requirements.

In mid-December, the US Congress passed the Consolidated Appropriations Act of 2021 (“CAA” or “Act”), which included another $900 billion in stimulus efforts tied to the COVID-19 pandemic. On December 27, 2020, President Trump signed the CAA into law. This article summarizes a number of provisions in the 5,593-page Act that are important to nonprofit organizations, including churches and church-related or private religious schools.

Review Church Law & Tax’s previous coverage regarding economic stimulus tied to the federal government’s COVID-19 pandemic response, and its effects on churches.

PPP Second Draw Loans

The CAA creates an extension of the Paycheck Protection Program (PPP) loan program with different eligibility requirements, which are outlined below. An additional $284 billion is available through these PPP Second Draw Loans.

Eligible borrowers

Before taking into account other limiting factors, note that eligible PPP Second Draw Loan borrowers include any:

Business concern;

Nonprofit organization (including a church);

Housing cooperative;

Eligible self-employed individual;

Sole proprietor; or Independent contractor.

A prior recipient of a PPP loan may apply for a PPP Second Draw Loan. However, an otherwise eligible applicant must also meet the following criteria:

Employ no more than 300 employees (this is a reduction from the 500 employees specified in the CARES Act passed back in March of 2020);

Have experienced a year-over-year reduction in gross receipts of not less than 25 percent when comparing any selected 2020 quarter to the equivalent 2019 quarter, excluding any funds received from a first PPP loan (note that the CAA has additional relevant details for entities that commenced operations in 2019 or between January 1, 2020, and February 15, 2020);

Not be otherwise excluded from receiving a US Small Business Administration (SBA) loan under other federal law (Chapter 13, Section 120.110 of the Code of Federal Regulations (CFR));

Not be engaged primarily in political or lobbying activities (which includes think tanks);

Not be owned by an entity formed in the People’s Republic of China or Hong Kong and which owns not less than 20% of the economic interest of the otherwise eligible borrower;

Not have as a member of its board of directors a person who is a resident of the People’s Republic of China; and

Not be a publicly traded company.

Maximum loan amount

The maximum PPP Second Draw Loan amount is computed as 2.5 times the average total monthly payment for payroll costs during 2019 or the one-year period before the loan is made, not to exceed $2 million.

For entities that began operations between February 15, 2019, and February 15, 2020, the maximum PPP Second Draw Loan amount is computed by first dividing the total monthly payments for payroll costs by the number of months in which those payroll costs were incurred or paid and then multiplying this quotient by 2.5, not to exceed $2 million.

Forgiveness of PPP loans of $150,000 or less

For PPP loans that do not exceed $150,000, including both PPP loans issued under the CARES Act and PPP loans issued under the CAA, borrowers may obtain forgiveness by submitting a certification to the lender which:

Is not more than one page in length;

Only requires the borrower to provide:

A description of the number of employees the borrower was able to retain because of the PPP loan;

The estimated amount the borrower spent on payroll costs; and

The total loan value.

Further, the borrower must certify that it accurately provided the required certification and complied with the PPP loan statute and regulations issued by the SBA. Finally, the borrower must retain employment records that prove compliance for four years and all other relevant records for three years. The borrower may voluntarily provide certain demographic information.

Church eligibility for PPP loans

The CAA makes clear that the SBA’s prohibition on making loans to religious organizations does not apply to PPP loans. In addition, the CAA expresses the sense of the Congress that the SBA’s previously issued Interim Final Rule properly clarified that the SBA’s affiliation rules do not apply to churches and religious organizations, where the application of those rules would substantially burden their free exercise of religion.

PPP loan forgiveness and EIDL grants

The CAA repeals the CARES Act provision requiring that any EIDL grant received would reduce the amount of PPP loan forgiveness.

Covered period redefined

The PPP loan Covered Period is redefined to begin on the date the loan originates (the date of a PPP loan’s first disbursement from the lender to the borrower) and end on a date selected by the borrower that is between the last day of the 8th week following the loan origination date and the end of the 24th week following the loan origination date. This change effectively permits a Covered Period that is between 8 weeks and 24 weeks rather than only permitting a Covered Period of 8 weeks or 24 weeks.

In addition, the Covered Period for PPP loans issued under the CARES Act may now extend to March 31, 2021, instead of December 31, 2020.

Changes to qualifying expenses

The CAA amends the CARES Act definition of qualifying benefits includible in payroll costs to include not only group health insurance benefits but also group life, disability, vision, or dental insurance benefits. This change applies to both PPP loans issued under the CARES Act and PPP loans under the CAA.

For PPP loans made under the CAA, the CAA adds to payroll costs, mortgage interest, rent, and utilities the following additional qualifying expenses:

Covered operations expenditures: Payments for any business software or cloud computing service that facilitates business operations; product or service delivery; the processing, payment, or tracking of payroll expenses; human resources; sales and billing functions; or accounting or tracking of supplies, inventory, records, and expenses.

Covered property damage costs: Costs related to property damage and vandalism or looting due to public disturbances that occurred during 2020 and was not covered by insurance or other compensation.

Covered supplier costs: Costs incurred for a supply of goods that are essential to the operations of the borrower at the time the cost is incurred and which were acquired pursuant to a contract, order, or purchase order in place at any time before the covered period or, in the case of perishable goods, in effect before or during the covered period.

Covered worker protection expenditures: Any operating or capital expenditure to facilitate the adaptation of the business activities of the borrower to comply with requirements established or guidance issued by the US Department of Health and Human Services, the US Centers for Disease Control, or the Occupational Safety and Health Administration, or any equivalent requirements established or guidance issued by a state or local government, during the period beginning on March 1, 2020, and ending the date on which the coronavirus national emergency expires, related to the maintenance of standards for sanitation, social distancing, or any other worker or customer safety requirement related to COVID-19. This may include the costs of installing or expanding: (i) an indoor, outdoor, or combined air or air pressure ventilation or filtration system; (ii) a physical barrier, such as a sneeze guard; (iv) additional indoor, outdoor, or combined business space; (v) an onsite or offsite health screening capability; or (vi) other assets to comply with federal or state coronavirus regulations or guidance. In addition, covered worker protection expenditures may include personal protective equipment (e.g., N-95 masks, surgical masks, nitrile gloves, and other similar items).

These additional qualifying expenses are not permitted to apply to the forgiveness of PPP loans obtained under the CARES Act.

Clarity regarding the tax treatment of qualifying expenses

The CAA clarifies that for taxable taxpayers, expenditures for PPP loan forgiveness qualifying expenses (i.e., payroll costs, mortgage interest, rent, and utilities) are fully deductible in computing taxable income. This overrides the position taken by US Treasury Secretary Steven Mnuchin and the Internal Revenue Service (IRS).

Unemployment provisions

Pandemic Unemployment Assistance

The CARES Act created a benefit called Pandemic Unemployment Assistance (PUA), which provided unemployment benefits to many individuals who otherwise failed to qualify for state unemployment benefits. Under the CAA, PUA now applies to “weeks of unemployment, partial unemployment, or inability to work caused by COVID-19 . . . ending on or before [March 14, 2021],” which extends the period of eligibility from December 31, 2020. Further, an eligible individual may receive PUA for 50 weeks, up from the 39 weeks permitted by the CARES Act. However, irrespective of the 50-week cap, the program ends effective April 5, 2021.

In addition, the CAA now requires applicants for PUA to provide proof of employment, self-employment, or the planned commencement of employment or self-employment to document eligibility for PUA. Further, recipients are required to recertify each week that they continue to be eligible for PUA.

Federal pandemic unemployment compensation

The CARES Act provided an additional federally funded $600 of unemployment compensation on top of any state unemployment compensation awarded. The CAA extends this benefit from December 26, 2020, through March 14, 2021, but at a reduced amount of $300.

CARES Act paid leave

Emergency paid sick leave

The CAA permits, but does not require, an employer to extend the emergency paid sick leave benefit created by the Families First Coronavirus Response Act (FFCRA) to March 31, 2021, and to continue to receive the credit against payroll taxes permitted by the FFCRA. The bill does not create new eligibility for the benefit.

Paid family leave

Similarly, the CAA permits, but does not require, an employer to extend the paid family leave provided under the FFCRA and to receive the credit against payroll taxes permitted by the FFCRA. The bill does not create new eligibility for the benefit.

Employee Retention Credit provisions

The CARES Act created an Employee Retention Credit (ERC). The credit was scheduled to expire on December 31, 2020. The CAA makes the following changes to the ERC:

Extends the ability to claim the ERC to wages paid before July 1, 2021;

Increases the ERC credit percentage from 50 percent to 70 percent for calendar quarters after December 31, 2020;

Retroactively eliminates to the enactment of the CARES Act the prohibition on obtaining a PPP loan and claiming the ERC. This effectively permits recipients of a PPP loan to retroactively claim the ERC; and

Increases the per-employee limitation from $10,000 for all calendar quarters to $10,000 for any calendar quarter after December 31, 2020.

Changed definition of a large employer

The CARES Act provided that for employers with more than 100 employees, qualified wages with respect to the ERC only included wages paid to employees not providing services. For employers with 100 or fewer employees, qualified wages included wages paid to all employees, regardless of whether an employee provided services. The CAA modifies this threshold to 500 employees, thereby increasing the number of employers eligible for the ERC. The change is effective for calendar quarters after December 31, 2020.

Gross receipts of an exempt organization

The CAA clarifies that for the purpose of computing the gross receipts of an exempt organization to determine whether an exempt organization is an eligible employer, the term “gross receipts” has the same meaning as the Internal Revenue Code’s Section 6033, the section that governs the filing of Form 990. This is defined as “the gross amount received by the organization during its annual accounting period from all sources without reduction for any costs or expenses.” This is the amount reported on Form 990, Part VIII, Line 12, column (A).

Editor’s note: Except for certain special situations, churches are not required to file an annual Form 990. Until further guidance is issued by the IRS, churches that are not required to file an annual Form 990 may consider using the computation method noted here for nonprofits that file a Form 990 to determine their eligibility as an employer.

Qualified disaster area ERC

The CAA adds a set of qualifying criteria to the ERC and modifies the credit amount in the case of an employer located in a qualified disaster area:

Credit amount: The credit amount is 40 percent of qualified wages, up to $6,000, paid by an eligible employer to an eligible employee. The $6,000 limit is reduced by any qualified wages taken into account in a prior taxable year.

Eligible employer: An eligible employer is any employer that conducts an active trade or business in a qualified disaster zone at any time during the duration of the qualified disaster and which trade or business is inoperable at any time during the qualified disaster as a result of damage sustained during the disaster.

Eligible employee: An employee of an eligible employer whose principal place of employment with the employer immediately before the qualified disaster is in the qualified disaster zone.

Qualified wages: Wages paid at any time on or after the date on which a trade or business located in a qualified disaster zone became inoperable at the principal place of employment of a qualified employee and before the earlier of (i) the date on which the trade or business resumed significant operations at that location, or (ii) 150 days after the last day of the disaster period. Qualified wages include wages paid without regard to whether the services are performed at the employee’s principal place of employment before significant operations resume, the employee performs services at a different principal place of employment, or the employee performs no services.

Special rules for exempt organizations: In the case of exempt organizations, the activities of the organization are deemed to be an active trade or business. In addition, the qualified disaster relief employee retention credit is allowed against the exempt organization’s employer Federal Insurance Contributions Act (FICA) tax obligation. The credit is only allowed to the extent of an employer’s quarterly FICA tax obligation. Any excess credit may be carried forward and claimed in the next calendar quarter. This credit is taken into account before the credits provided by the FFCRA for Emergency Paid Sick Leave and the Family Medical and Leave Act.

Education provisions

Elementary and Secondary School Emergency Relief Fund (ESSERF)

The CAA allocates $54.6 billion for elementary and secondary school coronavirus-related relief. The relief is allocated to each state educational agency with an approved application in the same proportion as its annual federal award. The funds may be used for a wide variety of purposes specified in the CAA.

Governor’s Emergency Education Relief Fund (GEERF)

The CAA provides $4.094 billion to be allocated among the governors of each state with an approved application. This fund provides funding to local public school authorities, including charter schools and higher education institutions, most impacted by the coronavirus and to non-public schools. Non-public schools may use funds granted for a wide variety of purposes enumerated in the statute, but all services or assistance provided, including equipment, materials, and any other items, must be secular, neutral, and non-ideological. A non-public school may not receive a PPP loan made after enactment of the CAA and a GEERF grant.

Miscellaneous provisions

Individual stimulus payments

The CAA authorizes recovery rebates (also known as “economic impact payments,” but more commonly referenced as the individual stimulus payments) in the form of a refundable credit of $600 per individual and $600 for each qualifying child of a taxpayer. This is a decrease from the $1,200 per individual under the CARES Act, but an increase in the “per child” amount, from $500 to $600. This credit is subject to eligibility and phase out per the following schedule (note that the phaseout ceiling increases by $12,000 for each qualifying child for which an economic income payment is received):

Filing Status

Full credit for Adjusted Gross Income less than or equal to:

No credit if Adjusted Gross Income exceeds:

Married filing joint

Surviving spouse

$150,000

$174,000

Head of house

$112,500

$124,500

Single

Married filing separate

$75,000

$87,000

Change in deductible floor for medical expenses

The CAA restores the floor for deducting medical expenses to 7.5 percent and makes this change permanent.

Extension of the Tax Cuts and Jobs Act of 2017’s paid family and medical leave credit

The Tax Cuts and Jobs Act of 2017 (TCJA) created an employer credit for up to two weeks of paid family and medical leave. This credit originally expired on December 31, 2019. It was subsequently extended to December 31, 2020. The CAA now extends the availability of this credit to December 31, 2025.

Extension of time for exclusion of employer payments of student loans from gross income

The CARES Act created an exclusion from an employee’s gross income for student loan payments made to an employee or a lender. This provision applied to such payments made before January 1, 2021. The CAA extends this exclusion to such payments made before January 1, 2026.

Extension of time to collect employee share of payroll taxes deferred under Notice 2020-65

Notice 2020-65 was issued in response to an August 8, 2020, Presidential Memorandum that in effect permitted employers to defer the collection of an employee’s share of FICA Medicare tax for wages received between September 1, 2020, and December 31, 2020. The notice then required an employer to collect the deferred FICA and Medicare tax from wages paid to the employee between January 1, 2021, and April 30, 2021. The CAA extends the deadline for collecting this tax from April 30, 2021, to December 31, 2021.

Extension of the above-the-line charitable deduction for non-itemizers

The CARES Act created a $300 above-the-line charitable deduction for cash charitable contributions by non-itemizers made during 2020 to public charities other than donor-advised funds described in Section 4966(d)(2) of the IRC and supporting organizations described in Section 509(a)(3) of the IRC. The CAA extends this deduction to cash contributions made after December 31, 2020, and further provides that in the case of contributions made after December 31, 2020, the deduction is $600 for married taxpayers filing a joint return.

Modification of limitations on charitable contributions

The CARES Act removed the adjusted gross income limitation on cash contributions made by individuals to public charities other than donor-advised funds described in Section 4966(d)(2) of the IRC and supporting organizations described in Section 509(a)(3) of the IRC, effectively permitting donors to deduct their 2020 cash contributions to the extent of their taxable income. Similarly, corporations were permitted to deduct cash contributions to the extent of 25 percent of their taxable income instead of 10 percent. The CAA extends these changes in the deductibility of charitable contributions to cash contributions made during 2021.

Carryover of Healthcare Flexible Spending Arrangement (HFSA) balances or Dependent Care Flexible Spending Arrangement (DCFSA) balances

In general, amounts placed in an HFSA or DCFSA must be expended by the end of the plan year, subject to a permitted grace period. The CAA provides that:

HFSA balances and DCFSA balances at the end of the 2020 plan year or 2021 plan year may be carried over;

The permitted grace period after the 2021 plan year may extend to December 31, 2022;

An employee who ceases to participate in an HFSA or DCFSA due to termination during calendar 2020 or 2021 may continue to seek reimbursement of unused HFSA or DCFSA balances through the end of the 2021 plan year, including any grace period that extends into 2022;

In the case where an employee enrolled in a DCFSA for a plan year in which the enrollment period ended on or before January 31, 2020, and the employee has a child who turned 13 during the plan year (i.e., aged out) and has a balance at the end of the plan year, the age at which the child will age out is increased to age 14 to permit the carryover of the unused balance; and

For the 2021 plan year, an employee may make a prospective election to modify the employee’s elective contributions to the FSA without regard to any change in status.

Note that these changes may require changes to your church or organization’s cafeteria plan document. Please seek legal counsel regarding amendments to the plan document.

Deduction of certain coronavirus-related expenses by elementary and secondary school teachers

Elementary and secondary school teachers are permitted to include amounts spent on personal protective equipment, disinfectant, and other supplies used for the prevention of the spread of the coronavirus as deductible educator expenses.

Coronavirus-related funeral expenses

Under a disaster relief provision, the bill provides financial assistance to an individual or household to pay for 100 percent of funeral expenses incurred through December 31, 2020, in connection with the emergency disaster declaration declared by President Trump on March 13, 2020.

Ted R. Batson Jr. is a CPA and tax attorney, and serves as a partner and Professional Practice Leader – Tax for CapinCrouse LLP, a national CPA and consulting firm. He speaks and teaches frequently for national conferences and organizations on exempt organization and charitable giving matters.

Key Tax Dates January 2021

Along with semiweekly and monthly requirements, note payroll tax rates for 2021 and review employee W-4s.

If your church or organization reported withheld taxes of more than $50,000 during the most recent lookback period (for 2021, the lookback period is July 1, 2019, through June 30, 2020), then the withheld payroll taxes are deposited semiweekly. This means that for paydays falling on Wednesday, Thursday, or Friday, the payroll taxes must be deposited on or by the following Wednesday. For all other paydays, the payroll taxes must be deposited on the Friday following the payday.

Note further that large employers having withheld taxes of $100,000 or more at the end of any day must deposit the taxes by the next banking day. The deposit days are based on the timing of the employer’s payroll. Withheld taxes include federal income taxes withheld from employee wages, the employee’s share of Social Security and Medicare taxes (7.65 percent of wages), and the employer’s share of Social Security and Medicare taxes (an additional 7.65 percent of employee wages).

Click image to download PDF

Monthly requirements

If your church or organization reported withheld taxes of $50,000 or less during the most recent lookback period (for 2021, the lookback period is July 1, 2019, through June 30, 2020), then withheld payroll taxes are deposited monthly. Monthly deposits are due by the 15th day of the following month.

Note, however, that if withheld taxes are less than $2,500 at the end of any calendar quarter (March 31, June 30, September 30, or December 31), the church need not deposit the taxes.

Instead, it can pay the total withheld taxes directly to the IRS with its quarterly Form 941. Withheld taxes include federal income taxes withheld from employee wages, the employee’s share of Social Security and Medicare taxes, and the employer’s share of Social Security and Medicare taxes.

January 1, 2021: Payroll Taxes

Social Security and Medicare taxes

Employees and employers each pay Social Security and Medicare taxes equal to 7.65 percent of an employee’s wages. The tax rate does not change in 2021.

The 7.65 percent tax rate is comprised of two components: 1) Medicare hospital insurance tax of 1.45 percent, and 2) an “old age, survivor and disability” (Social Security) tax of 6.2 percent. There is no maximum amount of wages subject to the Medicare tax.

The tax is imposed on all wages regardless of amount. For 2021, the maximum wages subject to Social Security taxes (the 6.2 percent amount) is $142,800. Stated differently, employees who receive wages in excess of $142,800 in 2021 pay the full 7.65 percent tax rate for wages up to $142,800, and the Medicare tax rate of 1.45 percent on all earnings above $142,800. Employers pay an identical amount. The Medicare tax rate for certain high-income taxpayers increases by an additional 0.9 percent.

Self-employment taxes

The self-employment tax rate (15.3 percent) does not change in 2021. The 15.3 percent tax rate consists of two components: 1) a Medicare hospital insurance tax of 2.9 percent, and 2) an “old age, survivor and disability” (Social Security) tax of 12.4 percent. There is no maximum amount of self-employment earnings subject to the Medicare tax.

The tax is imposed on all net earnings regardless of amount. For 2021, the maximum earnings subject to the Social Security portion of self-employment taxes (the 12.4 percent amount) is $142,800. Stated differently, persons who receive compensation in excess of $142,800 in 2021 pay the combined 15.3 percent tax rate for net self-employment earnings up to $142,800, and only the Medicare tax rate of 2.9 percent on earnings above $142,800.

These rules directly impact ministers, who are considered self-employed for Social Security with respect to their ministerial services. Ministers should take these rules into account in computing their quarterly estimated tax payments. The Medicare tax rate for certain high-income taxpayers increases by an additional 0.9 percent.

Federal incomes taxes

Beginning on this date, churches having nonminister employees (or a minister who has elected voluntary withholding) should begin withholding federal income taxes from employee wages. To know how much federal income tax to withhold from employees’ wages, employers should have a Form W-4 on file for each employee. Employees should file an updated Form W-4 for 2021, especially if they owed taxes or received a large refund when filing their previous tax return. Employees should use the IRS Tax Withholding Estimator to determine accurate withholding.

January 15, 2021: Fourth quarter estimated taxes due

Ministers (who have not elected voluntary withholding) and self-employed workers must file their fourth quarterly estimated federal tax payment for 2020 by this date (a similar rule applies in many states to payments of estimated state taxes).

Employees of churches that filed a timely Form 8274 (waiving the church’s obligation to withhold and pay FICA taxes) are treated as self-employed for Social Security purposes, and accordingly are subject to the estimated tax deadlines with respect to their self-employment (Social Security) taxes unless they have entered into a voluntary withholding arrangement with their employing church or organization.

Richard R. Hammar is an attorney, CPA and author specializing in legal and tax issues for churches and clergy.

Image: pinstock | Getty

Most Churches Remain Optimistic About Their Financial Outlook in the Coming Months

Still, around a third of all churches express uncertainty or pessimism as they look toward 2021.

The Editors

Cash donations to churches from January through September of this year were higher or holding steady for 58 percent of all churches when compared to giving in same period in 2019, according to a study of giving during the pandemic recently released by the Evangelical Council for Financial Accountability (ECFA).

This finding tracks closely with the giving trends noted in two studies conducted this past summer by the National Association of Evangelicals and the Lake Institute on Faith and Giving. The ECFA study surveyed 559 churches, along with 730 nonprofits, including both ECFA members and nonmembers, and was conducted from late October to early November.

This positive trend in giving is rather remarkable when considering that many churches had not been holding in-person gatherings due to the pandemic and the overall economy had been taking a beating and the unemployment rate continued to rise. On top of that, two-thirds of all churches in the study were actually optimistic about their financial outlook for 2021.

“Despite incredible challenges, 2020 has seen remarkable resiliency and significant forward motion among ECFA members and other like-minded ministries,” says ECFA’s vice president of research and equipping Warren Bird in the study’s report. “We were impressed by their strong optimism that God will continue to provide the funding needed to fuel gospel-motivated ministry.”

Along with giving, the study also covered a number of key areas related to church finances during the pandemic. Overall, the various findings in the ECFA study were similar for churches with the largest annual income ($10 million or higher) and the smallest annual income (under $500,000).

Staffing levels held their own

When it came to staffing during the third quarter of the year, 16 percent of churches reported a staff increase, with 67 percent reporting they were keeping their current staff size and 17 percent said they had to reduce staff. As they anticipated their fourth quarter, 9 percent of churches expected staff reductions, with 77 percent saying they would maintain current levels and 14 percent planning to add staff.

A surprising and hopeful finding was that plans in 2021 to increase staff bumped up to 28 percent, with 57 percent keeping staffing levels the same. Still, 15 percent were anticipating a reduction in staff.

Non-staff expense adjustments and positive plans for 2021

As the third quarter books closed, 36 percent of churches reported they had either increased or maintained non-staff expenses, while 64 percent had either postponed or reduced budgeted expenses (e.g., expanding a program or facility) or some type of service they would normally provide. Then, looking forward to the fourth quarter of the year, 53 percent of churches sought to increase or maintain such expenses while 47 percent anticipated either postponing or reducing such expenses.

However, the outlook for 2021 appeared brighter for 63 percent of churches as they anticipated either increasing spending or maintaining current spending; on the downside, 37 percent made plans to either postpone or reduce expenses.

ECFA’s Bird believes, however, these various adjustments to non-staff expenses are positive signs for many churches.

“Churches largely retained their staff, but cut or postponed other expenses during the summer,” Bird told Church Law & Tax. Additionally, Bird said that many pastors have told him that “with their facilities closed or minimally used for many months, their operational costs have been lower. Thus, cutting and postponing is not always something they were forced to do.”

Further, “the 64 percent that cut or postponed were speaking only of July through September, while 47 percent say they’ll cut or postpone for October through December, and 37 percent say that they’ll cut or postpone in 2021. That’s movement in a healthy direction.”

What about cash reserves?

Of those churches surveyed, 81 percent reported their cash reserves weren’t touched during the third quarter of the year. As those churches looked forward to 2021, however, with the continuing effects of the pandemic undoubtedly in mind, a little over half (54 percent) believed their reserves would still go untouched, with 41 percent saying they would most likely use some and 5 percent said they would use all of their cash reserves.

While two-thirds of those churches surveyed expressed optimism, a third were either uncertain or pessimistic about revenue going forward. And while 58 percent said donations were the same or higher from January through September, 42 percent reported giving was lower during that time period.

Regarding those struggling churches, ECFA’s Bird offered these insights:

Our research shows that those who were financially precarious going into the pandemic have especially felt it hard. Often the financial challenges are symptoms of underlying issues that can be addressed in healthy ways, such as clarifying God’s vision for this season in the life of the church, prayerfully discerning realistic steps to implement the vision, empowering and supporting more lay leaders, and mobilizing more people in the congregation for ministry.

Those churches that end up unable to weather this ongoing financial storm, Bird said:

A small percentage of churches may decide that they cannot make a comeback after the pandemic. Rather than closing, they might consider a merger. Church mergers are not only on the rise, but a much higher percentage of them are finding a whole new chapter of ministry as they partner with another church to begin the cycle of new life in Christ all over again.

Bottom line: In the coming months a number of churches will most likely be forced to make difficult decisions as the pandemic lingers into the early months of the new year.

On Demand Webinar: Tackling the Top Year-End Tasks for 2020

Richard Hammar reminds and informs church leaders about 10 important year-end tasks.

Featuring Richard R. Hammar, Attorney, CPA

Loading the player...

Church Law & Tax, renowned attorney, CPA, and senior editor Richard R. Hammar updates church leaders on key tasks for correctly handling business expenses, housing allowances, charitable contributions, and other issues—all to ensure 2020 ends strong, and 2021 begins well.

As a part of his presentation, Hammar also covers key developments related to COVID-19, including the CARES Act, and the tax-related implications the pandemic poses for churches, ministers, and congregants.

On December 1, the Small Business Administration (SBA) publicly released information about all Paycheck Protection Program (PPP) borrowers, including the name and address of each borrower, the exact amount of each borrower’s PPP loan, and the name of each borrower’s lender (among other data points).

The disclosure was made as a result of a federal court order to release the data in the public interest.

Public disclosure of this information will result in more scrutiny of PPP borrowers by the media and the general public. It will also likely result in numerous contacts by solicitors and fraudsters armed with specific information about borrowers and their loan amounts.

All PPP borrowers should remain on guard for the possibility of unscrupulous parties, many of them masquerading as legitimate companies or entities, contacting them by email or otherwise for nefarious purposes. Some fraudsters may attempt to create the false impression that they represent the borrower’s lender or the SBA itself.

This information originally appeared in the Batts Morrison Wales & Lee Special Alert e-newsletter. Used with permission.

Michael (Mike) E. Batts is a CPA and the managing partner of Batts Morrison Wales & Lee, P.A., an accounting firm dedicated exclusively to serving nonprofit organizations across the United States.

Image: GlobalStock |Getty

Recommended Reading

Protecting Children and Youth

Learn how to help keep kids safe, the right way to respond to allegations of abuse, and legal requirements related to reporting and screening.

The Editors

One of the perennial top reasons churches go to court each year is an allegation of abuse raised against a church volunteer, staff member, or pastor. Even with increased public outrage and calls for change in recent years, both inside and outside of the church community, the problem persists.